Watches and jewelry are a big category, If you want to know the potential of this market, then the prospects and future of this category should be reviewed

let’s dig it.

Market Insight of Watches & Luxury Watches

this is the total revenue of the watches & Jewelry industryWorldwide 2017-2026

Comments:the revenue increased significantly from 2017 to 2026, and is essentially flat during the covid-19 epidemic

Luxury Watches

Below will talk about the Luxury watches industry, Data sources are based on the following product ranges

Wristwatches

Pocket watches

Handmade and industrially produced watches

Market data

For Luxury Watches

A receita no segmento de Relógios de Luxo totaliza US$ 48,38 bilhões em 2023. O mercado deverá crescer anualmente 2,38% (CAGR 2023-2028).

Na comparação global, a maior parte das receitas é gerada na China (10.890,00 milhões de dólares em 2023).

Sobre os números totais da população, serão geradas receitas per capita de 6,30 dólares em 2023.

Comments:The luxury watches market is still worth entering or investing in

Revenue

Notes: Data shown is using current exchange rates and reflects market impacts of the Russia-Ukraine war.

Most recent update: Mar 2023

Comments:Market trend is still up

Revenue Change

Comments:Sales are decreasing, indicating that each brand should create its own special products, which can increase the unit price of sales

Average revenue per Capita

Most recent update: Mar 2023

Comments:To a certain extent, it shows that the per capita income has increased and people are willing to afford to buy luxury watches

This suggests that people are willing to spend more on watches and that the market is growing or becoming more profitable.

Several factors could contribute to the increase in average revenue per capita in the watches industry:

Economic Growth: A growing economy often leads to increased disposable income, allowing individuals to spend more on luxury goods like watches.

Shift in Consumer Preferences: If there has been a shift in consumer preferences towards luxury watches or specific watch brands, it can drive up the average revenue per capita as consumers are willing to pay higher prices for these products.

Product Innovation: Innovative features or designs in watches can attract customers and command higher prices, leading to increased revenue per capita.

Brand Value: Established watch brands with strong brand recognition and reputation can charge premium prices for their products, contributing to higher average revenue per capita.

Emerging Markets: Expansion into new markets or increased demand from emerging economies with a growing middle class can boost overall revenue and increase average revenue per capita.

Online Sales and E-commerce: The rise of e-commerce and online sales channels allows watch companies to reach a wider customer base and potentially increase their average revenue per capita.

These factors, among others, can contribute to the upward trend in average revenue per capita in the watches industry. However, it’s essential to consider specific market dynamics, consumer behavior, and industry trends to gain a comprehensive understanding of the underlying reasons for this increase.

Sales Channels

Most recent update: Oct 2021

Comments:People tend to buy watches online, so brands should establish a good online sales network, such as an online website or platform

Comments:When buying online, many people view through their cell phones, the adaptive website of each platform, the mobile version should be designed

Key Players

Most recent update: Mar 2022

Comments:Rolex and the Swatch group take up half of the watches industry’s market

Global Comparison

Most recent update: Mar 2023

Comments:China is still the biggest buyer of luxury watches, occupying a large market share, followed by the United States, brands should develop Chinese customers well

Key Market Indicators

Relógios

This watch contains a collection of smartwatches, digital watches, mechanical watches, quartz watches and various other watches

Data SCOPE of Watches segment

Relógios

Pocket watches

Analog and digital watches as well as smartwatches

Market data

For watches:

Revenue in the Watches segment amounts to US$75.75bn in 2023. The market is expected to grow annually by 4.44% (CAGR 2023-2026).

In global comparison, most revenue is generated in China (US$17,800.00m in 2023).

In relation to total population figures, per-person revenues of US$9.86 are generated in 2023.

By 2023, 60% of sales in the Watches segment will be attributable to Non-Luxury goods.

Comments:The watch market is still in growth mode

Revenue:

Notes: Data shown is using current exchange rates and reflects market impacts of the Russia-Ukraine war.

Most recent update: Jun 2022

Comments:Turnover is also growing

Comments:Change in turnover percentage and decrease in profit

watches -Average revenue per Capita is increasing

Most recent update: Jun 2022

Comments:Revenue per capita for watches is growing, indicating that people are willing to invest in watches

Luxury Revenue Share

Most recent update: Jun 2022

Comments:The revenue of luxury and non-luxury watches remains the same as before, people invest in non-luxury watches more than luxury watches, after all, the general public is the majority, non-luxury brands can still expand the market well

Sales Channels

Most recent update: Oct 2021

Comments:The online sales channel is still growing at a certain percentage

Comments:As people’s reliance on cell phones rises, the amount of cell phone purchases and watch browsing has been on the rise, Mobile applications in the market share has been going online and is expected to have a share of 59.8% in 2025

Key Players

Most recent update: Oct 2020

Comments:the Apple watch, Richemont, Rolex, and Swatch, 4 major brands occupy the main market, Apple smartwatches are still more popular.

Global Comparison

Most recent update: Jun 2022

Comments:China has become the largest market for luxury watches in the region due to the presence of high-net-worth individuals. The same, do not fail to think about the Chinese market customers.

Key Market Indicators

The following Key Market Indicators give an overview of the social and economic outlook of the selected region and provide additional insights into relevant market-specific developments.

Final Thought on Market Insight of Watches & Luxury Watches :

All data show that watches are a market worth investing in. Although the overall market economy is not very stable now, everyone is tightening their budgets and the purchasing power of non-essential consumer goods is declining, the building of a watch brand is a long-term process, so it is better to start slowly from now on.

However, the above data is not enough, let’s look at the worst times, under the impact of the epidemic, the market data

Overview Report of Watches & Jewelry 2020

In 2019, Watches and jewelry comprised 67% of the Accessories market, generating US$344.0 billion.

Let’s see the reports:

Relógios & Jewelry Overview

Market Definition

Jewelry and Watches are an essential part of the Watches & Jewelry segment

The Watches & Jewelry segment contains watches, pocket watches, stopwatches, and jewelry watches.

Moreover, the segment includes brooches, rings, necklaces, earrings, and bracelets made from most different materials.

The below data does not include: Watch parts, Watchbands, and Non-wearable fashion accessories

It includes: Analog and digital watches as well as smartwatches, Fashion, and high-jewelry

Key takeaways

In 2019, the Accessories market generated a total revenue of US$511.4 billion worldwide.

At 67%, Watches & Jewelry was the largest segment of the Accessories market with US$344.0 billion in revenues in 2019.

Key players in the Accessories market include Rajesh Exports Ltd., Compagnie Financière Richemont SA, Lao Feng Xiang Co., Ltd., Samsonite International SA, and Pandora AS

Worldwide revenue share in 2019

Worldwide Accessories revenue in billions of US$

Segment overview

In 2019, worldwide Watches & Jewelry sales amounted to US$344.0 billion

Key takeaways

The worldwide Watches & Jewelry revenue will increase at a CAGR1 of 1.5% from 2012 to 2025.

Due to COVID-19, the new 2020 forecast for the Watches & Jewelry segment is 15.9% lower than the original forecast.

In the Watches and jewelry segment, Hong Kong (US$976.5) and Singapore (US$307.5) had the highest annual revenue per capita in 2019.

Worldwide revenue in billions of US$

COVID-19 impact

Due to COVID-19, the 2020 forecast for the Watches & Jewelry segment is 15.9% lower now

Worldwide revenue in billions of US$1

Revenue share by subsegment

Jewelry generates the highest revenue in the Watches & Jewelry segment

Worldwide revenue in billions of US$

Accessories: top 10 companies by revenue

Rajesh Exports Ltd. had the highest total revenue of The top companies in the Accessories market

Regional Overview

Worldwide comparison

In 2019, people of Hong Kong and Singaporeans spent the most on Watches and Jewelry

Comment:HK has the best data because a lot of people from mainland China go to Hong Kong to buy luxury goods Hk most people buy those because Chinese mainland people always

Revenue per capita ranking in US$ in 2019

Revenue share in 2019

KPI comparison

KPI comparison – Europe (1/2)

Watches and jewelry sales in Europe will increase at a CAGR1 of 1.2% from 2012 to 2025

Revenue in billion US$

Revenue per capita in US$

KPI comparison – Europe (2/2)

In Europe, the UK was the country with the highest revenue in the Watches & Jewelry segment

Revenue ranking in billion US$ in 2019

Revenue per capita ranking in US$ in 2019

KPI comparison – Americas (1/2)

Watches and jewelry sales in the Americas will increase at a CAGR1 of 1.3% from 2012 to 2025

Revenue in billion US$

Revenue per capita in US$

KPI comparison – Americas (2/2)

In the Americas, the U.S. was the country with the highest revenue in the Watches and jewelry segment.

Revenue ranking in billion US$ in 2019

Revenue per capita ranking in US$ in 2019

KPI comparison – Asia (1/2)

Watches and jewelry sales in Asia will increase at a CAGR1 of 1.6% from 2012 to 2025

Revenue in billion US$

Revenue per capita in US$

KPI comparison – Asia (2/2)

In Asia, China was the country with the highest revenue in the Watches & Jewelry segment 7.

Revenue ranking in billion US$ in 2019

Revenue per capita ranking in US$ in 2019

KPI comparison – Africa (1/2)

Watches and jewelry sales in Africa will increase at a CAGR1 of 3.9% from 2012 to 2025

Revenue in billion US$

KPI comparison – Africa (2/2)

In Africa, Nigeria was the country with the highest revenue in the Watches & Jewelry segment

Revenue ranking in billion US$ in 2019

Revenue per capita ranking in US$ in 2019

KPI comparison – Australia & Oceania (1/2)

Relógios & Jewelry sales in Australia & Oceania will increase at a CAGR1 of 0.5% from 2012 to 2025

Revenue in billion US$

Revenue per capita in US$

KPI comparison – Australia & Oceania (2/2)

In Australia & Oceania, Australia was the country with the highest revenue in the Watches & Jewelry segment

Revenue ranking in billion US$ in 2019

Revenue per capita ranking in US$ in 2019

Top countries by region

In the UK, the Watches & Jewelry segment will grow by 13.0% from 2019 to 2025

Revenue in the top countries in billions of US$

Consumer Insights

Analyst Comments

The growing popularity of smartphones has hampered the growth of the watch industry

Trends

▪ The growing usage and popularity of smartphones have replaced the basic functionality of watches.

▪ The substituting effect of smartphones hampered the growth of the watch industry.

▪ Manufacturers are increasingly marketing watches as a fashion accessory, which appeals to only a limited section of society.

▪ The jewelry market has also witnessed only tepid growth, owing to factors such as the growing popularity of imitation jewelry due to its cost advantages.

Sales channels

Online retail‘s share of Accessories reached19.6% in 2019

Accessories: worldwide revenue share

Comment:The percentage of Online revenue is increasing year by year, if you still have no online channel, You can try one now.

COVID-19 impact on eCommerce

In 2020, consumers have shifted to purchasing clothing online in all major e-commerce markets

Online instead of offline purchases related to the COVID-19 pandemic

Top eCommerce stores

Vip.com was the biggest online retailer specializing in Fashion globally in 2019

Biggest players with Fashion as their main product category in 2019

Pensamento final

As we reflect on the Watches and jewelry market in 2020, it’s clear that this industry, while resilient, has encountered significant challenges, notably from the rise of smartphones and the shifting landscape of consumer preferences. However, it also demonstrates adaptability, with manufacturers repositioning watches as fashion accessories and the enduring allure of high-quality jewelry. the jewelry and jewelry industry is a potential industry worth investing in.

China has established itself as a prominent hub for the watch industry, hosting several renowned watch fairs and exhibitions. These events serve as pivotal platforms for watch enthusiasts, retailers, and brands to explore the latest trends, network with industry experts, and discover potential suppliers.

In this section, we delve into the significance of China’s watch fairs and how they can be instrumental in your watch sourcing journey.

here’s a list of some well-known watch fairs in China:

China Watch & Clock Fair (CWCF)

Shenzhen Watch & Clock Fair

Hong Kong Watch & Clock Fair (although technically in Hong Kong, it’s in close proximity to mainland China and is a significant event for the industry)

Shanghai Watch Fair

Beijing Watch Fair

Guangzhou Watch Fair

These fairs are instrumental in the watch industry and offer excellent opportunities for sourcing and networking within the watch business.

Top Watch Fairs In China

The China Watch & Clock Fair (CWCF):As one of the largest watch fairs in Asia, the CWCF draws exhibitors and attendees from around the world. It showcases a diverse range of watch styles, from luxury timepieces to affordable fashion watches.

Shenzhen Watch & Clock Fair:Known as one of the most influential watch events in China, the Shenzhen Watch & Clock Fair specializes in showcasing cutting-edge technologies and innovations in the watch industry.

Key Benefits of Attending China’s Watch Fairs

Exposure to a Wide Range of Suppliers:These fairs bring together a multitude of watch suppliers, making it a one-stop destination to explore a diverse array of products.

Networking Opportunities:China’s watch fairs offer unparalleled networking opportunities, allowing you to connect with watch manufacturers, designers, and other industry professionals.

Insights into Market Trends:Stay updated on the latest market trends, technological advancements, and consumer preferences by attending seminars and presentations at these fairs.

Hands-on Experience:Get a firsthand look at the quality and craftsmanship of watch products, enabling you to make informed decisions about potential suppliers.

Negotiation Advantage:Face-to-face interactions with suppliers often provide a negotiation advantage, allowing you to discuss pricing, bulk orders, and customization options.

Tips for Maximizing Your Experience at China’s Watch Fairs

Preparation is Key:Research the fair’s exhibitors, layout, and schedules in advance to make the most of your time.

Check the Quality/ buy sample:Get to know your watch supplier by verifying their quality, this is the fastest way, also in China watch fairs, It’s allow you to buy samples directly. Try it.

Bring Your Business Cards:Networking is essential; ensure you have a stack of business cards to exchange with potential suppliers and partners.

Engage in Conversations:Don’t hesitate to strike up conversations with exhibitors and fellow attendees. You may discover valuable insights or partnership opportunities.

Take Notes and Catalogs:Carry a notebook to jot down important details and collect catalogs from suppliers for reference.

How to Communicate with China Watch Fair Suppliers?

Talking with watch fair suppliers is a crucial part of your interaction when attending a watch fair in China. Effective communication can help you establish valuable connections and gather essential information. Here are some tips on how to talk with watch fair suppliers:

Research in Advance:Before attending the fair, research the suppliers and exhibitors who will be present. Identify the ones that align with your business needs and objectives.

Prepare Your Questions:Have a list of questions ready. These questions could be about their product range, manufacturing capabilities, quality control processes, lead times, and pricing.

Engage Actively:Approach suppliers with a friendly and professional demeanor. Smile, make eye contact, and give a firm handshake when appropriate. Engage in small talk to build rapport before diving into business discussions.

Introduce Your Business:Start the conversation by introducing your own business, its goals, and what you are looking for at the fair. This helps suppliers understand your needs better.

Ask About Their Offerings:Inquire about the products they offer. Ask for details about materials, designs, and any unique features. Seek to understand how their products can benefit your business.

Quality Assurance and Certifications:Ask about their quality control processes and any certifications they hold. This is crucial for ensuring the quality of the products you intend to source.

Pricing and MOQ (Minimum Order Quantity):Discuss pricing structures and MOQs. Be clear about your budget and quantity requirements. Negotiate prices if necessary, but do so respectfully.

Lead Times and Delivery:Understand their lead times and delivery schedules. This is important for planning your inventory and ensuring timely product availability.

Samples and Catalogs:Request product samples and catalogs for your reference. These materials can help you make informed decisions and compare different suppliers.

Language Considerations:If you don’t speak Mandarin Chinese, consider bringing a translator or utilizing translation apps to facilitate communication. Many suppliers may have English-speaking representatives as well.

Take Notes:Jot down key information during your discussions. This will help you keep track of different suppliers’ offerings and details.

Exchange Contact Information:Before concluding your conversation, exchange contact information, including business cards. This allows you to follow up after the fair.

Be Respectful of Their Time:Remember that suppliers may be interacting with numerous attendees. Be respectful of their time and avoid monopolizing their attention if the conversation is not relevant to your needs.

Follow-Up After the Fair:After the fair, follow up with the suppliers you are interested in working with. Send them emails or make phone calls to continue discussions and finalize agreements.

Remember that building relationships with suppliers takes time, so approach conversations with patience and a genuine interest in finding the right partners for your watch business.

More Benefits of attending the China’s Watch Show

China’s watch fairs stand as multifaceted events that cater not only to watch manufacturers but also to watch component suppliers, middlemen, distributors, and even renowned watch brands. These exhibitions serve as pivotal gatherings in the world of horology, offering a wide array of opportunities and resources for industry professionals. Let’s delve deeper into the diverse facets of China’s watch fairs:

Inclusive Participant Pool:China’s watch fairs boast a diverse participant pool. While watch manufacturers showcase their latest creations and innovations, a significant presence is also maintained by watch component suppliers who provide essential parts and mechanisms for the watchmaking process. Furthermore, middlemen, traders, and even established watch brands participate actively in these events. This eclectic mix of participants makes China’s watch fairs a one-stop destination for the entire spectrum of the watch industry.

Beyond Sourcing:Attending these fairs goes far beyond merely finding new suppliers. They serve as windows into the ever-evolving watch market. Suppliers often use these events to showcase their latest and most exceptional products, allowing attendees to gain firsthand insight into the newest trends, designs, and technological advancements in the watch industry.

Assessment of Supplier Strength:Participation in these fairs is not to be taken lightly. The costs associated with setting up an exhibition booth at a major Chinese watch fair can range from tens of thousands to several hundred thousand dollars. This significant investment means that participating suppliers are often well-established and financially robust. Their presence at these fairs is a testament to their commitment to the industry.

Local and International Blend: While local suppliers primarily dominate these fairs, they are increasingly attracting international attention. This international flavor is a testament to China’s growing importance in the global watch industry. Attendees from around the world converge at these fairs to explore business opportunities and discover unique watchmaking talents.

Opportunities for Company Visits:For those who have the opportunity and the time, it’s possible to arrange visits to the manufacturing facilities of the exhibiting suppliers. This allows for a more in-depth understanding of their production processes, quality control measures, and overall capabilities.

Given the rich diversity of participants, the showcase of cutting-edge products, and the networking opportunities, it’s advisable to allocate sufficient time and resources when planning a trip to China for these watch fairs. This ensures that you can fully capitalize on the multifaceted opportunities they present.

Conclusion:

China’s watch fairs play a pivotal role in the global watch industry, offering many opportunities for sourcing high-quality timepieces, establishing valuable connections, and staying informed about market developments. By strategically participating in these fairs, you can position your brand for success in the competitive world of watch retail and distribution.

When selecting a watch brand, style, and model, do you find yourself overwhelmed by the choices? This is because there are numerous watch brands available. However, many of these brands are part of the 4 majorwatch Giant Companies.

The 4biggest watch giants Companiesin the world, areSwitzerland’s Swatch Group, the Rolex Group, the Swiss’s Richemont Group, and France’s Louis Vuitton (LVMH) Group.

We’ll take a closer look at the strategies they use, their diverse products, and the core philosophies behind their brands to see what sets each one apart in shaping the industry.

What Are the Big 4 Watch Brands?

The world’s 4 major watch groups typically refer to the four companies with the largest scale and widest influence in the global watch industry. They are:

Swatch Group: Headquartered in Switzerland, it owns several famous brands, including Blancpain, Omega, Tissot, Longines, and Swatch.

Richemont Group: Also a Swiss luxury goods company, it includes many high-end watch brands such as Cartier, Vacheron Constantin, Jaeger-LeCoultre, and Piaget.

Rolex: An independent Swiss watch manufacturer known for its high quality and precision, Rolex is a sparkling star among global watch brands.

LVMH (Moët Hennessy Louis Vuitton): Headquartered in Paris, France, this renowned luxury group owns famous watch brands including TAG Heuer, Breguet, Chopard, and Hublot.

These groups not only possess multiple watch brands but also cover various market segments from entry-level to high-end luxury, holding significant shares in the global market.

These 4 brands have managed to maintain prominent positions in the watch market due to their heritage, innovation, and consistent delivery of quality and luxury.

At present, the amount of sales of high-end wristwatches is still Rolex, Richemont, Swatch and Louis Vuitton’s world ranking is far ahead. The watch exports of the Rolex, Swatch, and Richemont groups already account for more than 80% of all Swiss watch exports.

Company Brief and Brand Profile of the 4 Watch Giants

Richemont Group

Richemont is a Swiss luxury goods company that was established by South African billionaire Anton Rupert in 1988. The company’s business covers four main areas: jewelry, watches, accessories, and fashion.

Richemont banner

Watches are just one of the company’s business areas, as the group covers tobacco, fashion, leather goods, writing instruments, etc. Richemont’s watch brands are mostly top-of-the-line and are compatible with German, Swiss, Italian, and French brands.

Richemont considers itself the leader in watches for good reason, with a market share second only to the Swatch Group. Its Vacheron Constantin, Jaeger-LeCoultre, Panerai, Cartier, and Universal are very high visibility, while Jaeger-LeCoultre for the group provides some movements and technical support,

Piaget was the earliest development of the Swiss manufacturers of electronic quartz movement, but Switzerland’s few manufacturers continue to produce quartz movement in the field of the movement to specialize in ultra-thin movement., Piaget’s unique German style and the production of the perpetual calendar in the industry is also very famous! Piaget’s unique German style and perpetual calendar production are also famous in the industry.

Richemont categories

Richemont Group owns several prestigious watch brands, including:

Cartier

IWC Schaffhausen

Jaeger-LeCoultre

Panerai

Piaget

Vacheron Constantin

Montblanc

Baume & Mercier

Roger Dubuis

Van Cleef & Arpels (also known for jewelry)

These brands are renowned for their craftsmanship and luxury in the watchmaking industry.

Rolex

Rolex homepage display

Recognized universally, Rolex is synonymous with luxury and reliability in timekeeping. It has remained an independent company with a reputation for high-quality craftsmanship and iconic designs such as the Submariner, Daytona, and Oyster Perpetual.

The Rolex Group primarily owns two watch brands:

Rolex

Tudor

Both brands hold a very prestigious reputation and position in the global watch market.

LVMH (Louis Vuitton Moët Hennessy)

LVMH is the world’s largest luxury goods group, formed in 1987 by Bernard Arnault’s merger of Louis Vuitton, the world-famous leather goods company, and Moët Hennessy, the wine family, with more than 50 brands.

Involved in areas such as liquor, fashion, leather goods, cosmetics, watches, and jewelry, the LVMH Group is the world’s fourth-largest watch manufacturer.

Compared to Richemont and Swatch Group, LVMH’s main focus is not on the watch industry, and even if this is just a branch of their business, they have managed to jump to the top four groups

LVMH, founded in 1987, stands as a global luxury conglomerate with an unparalleled reputation for premium goods. LVMH is a conglomerate of luxury brands, known for its iconic fashion, jewelry, and watch brands like Louis Vuitton, TAG Heuer, and Bulgari.

LVMH blends traditional craftsmanship with contemporary innovation, offering a range of timepieces that cater to diverse tastes and preferences. With a focus on exclusivity and exceptional quality, LVMH’s watches often reflect the essence of timeless elegance.

Watches from LVMH brands are often positioned as high-end products, incorporating precious materials, advanced watchmaking technology, and meticulous design.

lvmh categories of watches

The watch brands owned by various groups and their founding years, including those primarily focused on watchmaking as well as those known for fashion watches, are as follows:

Hublot: Founded in 1980, Hublot is well-known for its innovative use of materials and distinctive design philosophy.

Zenith: Established in 1865, Zenith is renowned for its precision and craftsmanship in watchmaking.

TAG Heuer: Started in 1860, TAG Heuer is famous for its ties to auto racing and chronograph watches.

Dior Watches: Although Dior, founded in 1946, is primarily known for luxury fashion, its watch division creates high-fashion timepieces complementing its clothing lines.

Fred: Founded in 1936 as a jewelry brand, Fred also includes watches that blend jewelry craftsmanship with timekeeping.

Chaumet: Established in 1780, Chaumet, a jewelry house, offers luxurious timepieces that showcase its heritage in jewelry excellence.

Bvlgari: Since 1884, Bvlgari has been recognized for its bold jewelry and also offers watches that reflect its luxury style.

Corrections and additional details:

Diorwas founded in 1946, not 1985.

Louis Vuitton (LV), mentioned in the inquiry, is known for luxury goods, including fashion and leather goods, and has expanded into watches. It was founded in 1854.

Brands like Dior, LV, Bvlgari, and others you mentioned diversify their legacy of luxury through both high-end jewelry and fashion watches designed to complement wardrobe choices, marking them as fashion-forward pieces with a focus on aesthetic appeal.

Overall, while Hublot, Zenith, and TAG Heuer are primarily focused on the craft of watchmaking, brands like Dior, Bvlgari, and Chaumet excel in creating watches that serve as fashion statements, combining their heritage in luxury with functional elegance.

LVMH’s watch brands range from mid-tier to ultra-luxury, with prices spanning a wide spectrum to cater to different luxury segments.

Swatch Group

In 1985, the legendary Nicolas G. Hayek, after reorganizing Asuag and SSIH for more than four years, ultimately led to the merger of the two watch companies to form the Swatch Group.

The Swatch Group is the world’s largest watch manufacturer and distributor, and the only luxury goods group to specialize in watches. The Swatch Group has 160 manufacturing centers around the world and accounts for 25% of the world’s watch market in terms of retail sales.

Swatch Group has reshaped the watch industry through its diverse portfolio of brands. Swatch Group with several large groups is different, for all kinds of people to launch a different price point of the brand, it is known for its range of affordable and stylish watches, such as Tissot, Medo, Longines to go is the pro-people route. encompassing brands, From the playful Swatch to the precision of Omega and the prestige of Breguet, Swatch Group covers an extensive spectrum.

Renowned for its technical expertise and Swiss watchmaking heritage, the group has consistently pushed the boundaries of innovation while maintaining a strong connection to tradition.

It caters to both fashion-conscious and sports-oriented consumers, offering a mix of price points and styles.

Here are the watch brands:

OMEGA

Breguet

Blancpain

Jaquet Droz

Glashutte Original

Leon Hatot

Swatch

Longines

Rado

Tissot

Calvin Klein

Certina

Mido

Hamilton

Pierre Balmain

Flik Flak

Laco

Endura

Tissot offers a balance of style and affordability, appealing to those seeking quality Swiss watches. Longines, with its heritage and elegance, caters to a more classic and sophisticated audience. In the luxury segment, Omega and Breguet represent the pinnacle of Swiss watchmaking.

Swatch specializes in a variety of watches, including colorful and playful Swatch watches, classic Tissot timepieces, and high-end luxury watches under brands like Omega and Longines.

Swatch offers a broad range of price points, starting from affordable Swatch watches to high-end luxury watches from brands like Omega.

Innovation and Technology of the 4 Watch Giants

Richemont

Here’s an overview of how innovation and technology play a role within Richemont and its brands:

Materials Innovation: Richemont brands are known for their exploration and adoption of advanced materials. For instance, IWC Schaffhausen has integrated the use of Ceratanium® in their watch cases, combining the best properties of titanium and ceramic to offer remarkable durability and scratch resistance. Similarly, Panerai has introduced materials like Carbotech™ and BMG-Tech™, pushing the envelope in terms of aesthetics, durability, and lightweight properties.

Horological Innovations: Richemont brands have been pioneers in the development of horological innovations to improve the accuracy, functionality, and reliability of their timepieces. For example, Cartier’s development of the mystery clock and its more recent mystery movements in watches where the hands appear to float without any connection to the movement are feats of engineering. Jaeger-LeCoultre’s Gyrotourbillon offers a multi-axis tourbillon that compensates for errors in timekeeping due to gravity in all positions.

Sustainability Efforts: Across its portfolio, Richemont has increasingly integrated sustainability into its innovation strategy. Brands like Van Cleef & Arpels and Cartier are committed to responsibly sourced materials, including diamonds and gold. These efforts extend to reducing environmental impact through energy-efficient manufacturing processes and sustainable packaging solutions.

Digital Transformation: Richemont has actively embraced digital innovation to enhance customer experiences and operational efficiency. This includes the development of advanced e-commerce platforms, the use of virtual reality (VR) and augmented reality (AR) in product presentation and customer service, and the adoption of blockchain technology for product authentication and supply chain transparency. The acquisition of online platforms like Watchfinder & Co. reflects Richemont’s strategy to strengthen its position in the digital space.

Research & Development: Through dedicated R&D efforts, Richemont brands foster innovation in watchmaking and jewelry. This includes the invention of new mechanical movements, development of novel jewelry settings that offer both aesthetic appeal and functionality, and the exploration of cutting-edge manufacturing techniques.

Collaborations and Partnerships: Richemont has engaged in collaborations and partnerships with technology companies and startups to explore new avenues for innovation. Whether it’s through the integration of smart technology into traditional watchmaking or exploring new retail technologies, these collaborations keep Richemont at the forefront of innovation in the luxury sector.

Watchfinder & Co.: Recognizing the potential in the pre-owned watch market, Richemont acquired Watchfinder & Co., which leverages data analytics and technological solutions to authenticate and refurbish pre-owned watches, ensuring their quality and reliability.

Richemont’s approach to innovation and technology demonstrates a commitment to preserving traditional craftsmanship while embracing modern technologies and practices. This balance ensures that Richemont and its brands remain leaders in the luxury goods industry, perpetuating a legacy of excellence, sustainability, and innovation.

Rolex

Rolex is widely recognized for its significant contributions to innovation and technology in the watchmaking industry. Throughout its history, Rolex has introduced some technological advancements and features that have set industry standards and affirmed its reputation for quality and reliability. Some of these innovations include:

Oyster Case (1926): Rolex introduced the world’s first waterproof wristwatch case called the “Oyster.” This innovation provided the watch with superior protection against water and dust, greatly enhancing durability and reliability.

Perpetual Movement (1931): Rolex unveiled the first self-winding wristwatch mechanism with a perpetual rotor. This technology allowed the watch to be powered by the wearer’s movements, eliminating the need for manual winding.

Datejust (1945): The Rolex Datejust was the first wristwatch to feature a date function that automatically changed at midnight. This innovation was significant as it improved timekeeping convenience and functionality.

Submariner (1953): The Rolex Submariner was introduced as the first wristwatch waterproof to a depth of 100 meters (330 feet). Over the years, Rolex has continued to improve its water-resistant technology, with some models now waterproof to a depth of 3900 meters (12,800 feet).

GMT-Master (1955): The GMT-Master was developed to meet the needs of international pilots. It featured a 24-hour display fourth hand and a rotating bezel, allowing wearers to read the time in two different time zones simultaneously.

Day-Date (1956): Rolex introduced the first wristwatch that displayed both the date and the day of the week spelled out in full. This was particularly useful for international business and diplomatic activities.

Oysterquartz (1970s): In response to the quartz crisis, Rolex developed its own quartz movements for the Oysterquartz models. These were some of the most accurate quartz watches due to their high-quality quartz movements.

Materials Innovation: Rolex has also excelled in materials innovation, developing its own alloys such as 904L stainless steel, which offers higher resistance to corrosion, and Rolesor, a combination of 904L steel and 18kt gold. Additionally, Rolex developed Cerachrom bezels, made from a hard ceramic material that is resistant to scratching and fading.

Parachrom Hairspring and Paraflex Shock Absorber: Rolex developed the Parachrom hairspring, which is highly resistant to shocks and magnetic fields, enhancing the movement’s accuracy and reliability. The Paraflex shock absorber increases the movement’s shock resistance.

Rolex’s commitment to innovation is a key aspect of its legacy, constantly pushing the boundaries of what is possible in watchmaking to enhance precision, durability, and functionality.

LVMH

LVMH’s commitment to innovation is evident through its watch brands that push the boundaries of technology. TAG Heuer’s “Connected” series exemplifies LVMH’s foray into smartwatches, seamlessly merging luxury with digital functionality.

Zenith’s “Defy” line showcases advancements in precision through high-frequency movements, while Hublot’s “Art of Fusion” philosophy combines traditional watchmaking with avant-garde materials like ceramic, carbon, and sapphire. These innovations reinforce LVMH’s position as a trailblazer in merging luxury with cutting-edge technology.

LVMH’s brands, such as TAG Heuer, are known for innovation, incorporating advanced materials and technologies like tourbillons and chronographs into their luxury timepieces.

Swatch Group

Swatch Group’s emphasis on innovation can be seen through its advancements in materials and movements. Swatch’s playful designs are complemented by innovations in lightweight plastic cases and creative dial designs. Omega’s “Master Chronometer” certification highlights the precision and anti-magnetic properties, while Breguet’s technical prowess includes high-frequency movements and intricate tourbillons.

Swatch Group’s technological innovations uphold Swiss watchmaking’s reputation for precision and reliability.

Swatch is known for introducing innovative materials and technologies, including automatic movements, colorful designs, and limited-edition releases.

Check their website to get more information: https://www.swatchgroup.com/en/swatch-group/innovation-powerhouse

Each of these watch industry leaders demonstrates a distinct approach to innovation and technology, influencing the evolution of horology by embracing new materials, movements, and functionalities.

Market Presenceof the 4 Watch Giants(Retail and Distribution Strategies)

Check their global market presence of each company, including market share, geographical reach, and their influence on the watch industry.

Check how each company approaches distribution and retail, including its online presence, brick-and-mortar stores, and engagement with consumers.

Richemont

Rolex

LVMH

LVMH’s luxury watch brands operate a selective distribution approach, focusing on high-end boutique experiences. Flagship stores in prime global spots provide custom service and exclusive timepiece collections. Authorized dealers also reflect the brand’s upscale image, ensuring a uniform luxury retail experience.

With its worldwide boutique network and select retailers, LVMH’s presence spans major cities and top-tier shopping locales. The group’s cachet radiates beyond watches, enhancing its allure across the luxury and fashion sectors.

there are 36 Zenith stores and boutiques in ChinaTag Heuer stores all over the world

Swatch Group

Swatch Group adopts a multi-tiered distribution approach to cater to different market segments. Brands like Swatch have a wide retail presence, with standalone stores in shopping centers and high-traffic areas.

Omega, Longines, and Tissot maintain a combination of boutiques and authorized dealers, offering customers an opportunity to explore the brand’s offerings in diverse settings. This strategy allows Swatch Group to balance luxury boutique experiences with broader accessibility.

Swatch Group’s market presence is characterized by a diverse brand portfolio catering to different market segments. The approachable Swatch brand has a wide reach, with stores in urban centers and malls, targeting fashion-conscious individuals.

Longines and Tissot have a global footprint, appealing to those seeking Swiss quality at various price points. Omega’s association with sports, space exploration, and high-profile events solidifies its status in the luxury watch market.

These companies’ diverse strategies contribute to their distinct market presences, ranging from luxury exclusivity to widespread accessibility, each catering to different consumer demographics and preferences.

Design Philosophy Brand Imageof the 4 Watch Giants

LVMH:

LVMH’s watch brands are characterized by their commitment to luxury and elegance. The design philosophy revolves around timeless aesthetics, exquisite craftsmanship, and attention to detail. TAG Heuer embodies sportiness and precision, often incorporating bold and dynamic elements into its designs.

Zenith captures classic sophistication through its clean lines and refined dials.Hublot’s avant-garde “Art of Fusion” approach merges traditional watchmaking with modern materials, resulting in bold, statement-making timepieces. Overall, LVMH’s watch brands convey an image of opulence and exclusivity.

Hublot use 18k gold to make watch

LVMH’s watch brands are associated with prestige, luxury, and a sense of heritage. They appeal to consumers seeking status and elegance.

Swatch Group:

Swatch Group’s brand image varies across its diverse portfolio. Swatch stands for colorful creativity and affordability, appealing to the fashion-conscious and young at heart.

Tissot showcases a blend of style and value, catering to those seeking quality Swiss watches without the luxury price tag.

Longines exudes elegance and heritage, reflecting a classic aesthetic with a touch of modernity.

Omega signifies precision, innovation, and a connection to exploration and iconic events like theOlympicsand space missions.

Breguet embodies timeless elegance and intricate craftsmanship, appealing to connoisseurs of horological artistry.

Swatch is synonymous with colorful and playful designs, appealing to consumers looking for affordable yet stylish timepieces.

Brand Portfolioof the 4 Watch Giants

Discuss the various watch brands owned by each conglomerate, highlighting the uniqueness and individuality of each brand under the larger umbrella.

LVMH

LVMH’s watch division encompasses a range of prestigious brands, each with its own identity and appeal.

TAG Heuer,renowned for its precision and sporty aesthetics, targets enthusiasts of motorsports and athletics.

Zenith,a beacon of Swiss watchmaking excellence, offers classic and refined timepieces for aficionados of timeless elegance.

Hublot,known for its fusion of luxury and modern materials, captures attention with its bold and avant-garde designs.

These distinct brands within LVMH’s portfolio cater to a diverse audience, covering various style preferences and luxury levels.

Swatch Group:

The Swatch Group’s brand portfolio is a symphony of diversity, catering to a broad spectrum of consumers. Swatch, celebrated for its colorful and affordable designs, captures the youthful and fashion-forward market.

Tissotstrikes a balance between style and value, appealing to those seeking quality Swiss watches.

Longinesembodies timeless elegance with a modern touch, targeting individuals who appreciate classic sophistication.

Omega, with its legacy of precision and innovation, caters to luxury enthusiasts, while Breguet epitomizes horological craftsmanship and heritage for connoisseurs seeking artistic masterpieces.

In summary, LVMH, Fossil, and Swatch cater to different segments of the watch market, with varying brand positioning, product ranges, and price points. Understanding these differences can help you position your watch manufacturing business effectively within the broader landscape of the watch industry.

Influential Collaborations and Partnershipsof the 4 Watch Giants

Showcase notable collaborations and partnerships that have helped these companies gain visibility and connect with different consumer segments.

LVMH (Moët Hennessy Louis Vuitton):LVMH’s watch brands have engaged in partnerships that blend luxury with various industries.

TAG Heuerpartnered with Intel and Google to create the TAG Heuer Connected smartwatch, fusing Swiss craftsmanship with cutting-edge technology.

Hublotcollaborated with Ferrari, resulting in timepieces that embody the spirit of high-performance racing.

Zenithcelebrated its 50th anniversary of the iconic El Primero movement with a collaboration with Phillips Auction House, creating a limited edition series of watches that merged horological heritage with collectible appeal.

Swatch Group:Omegahas a storied history of collaborations, notably with NASA for the Moonwatch worn during moon landings. The brand’s partnership with the James Bond film franchise has solidified its association with sophistication and spy-worthy gadgets.

Longines is the official timekeeper for equestrian events and has collaborated with the equestrian world through various competitions. Tissot’s partnership with the NBA reflects its commitment to precision and sportsmanship, producing special edition watches for basketball fans.

Influential collaborations and partnerships have allowed these companies to tap into different industries, extending their brand reach and offering unique, limited-edition timepieces that capture the essence of their respective collaborations.

Sustainability Initiatives

Investigate the sustainability efforts undertaken by these industry leaders, including their approaches to responsible sourcing, manufacturing practices, and environmental impact.

LVMH (Moët Hennessy Louis Vuitton):

LVMH places emphasis on sustainability across its watch brands. TAG Heuer introduced the “Green Heuer” initiative, focusing on reducing the brand’s carbon footprint and incorporating eco-friendly materials. Zenith prioritizes responsible sourcing of materials, aiming to minimize environmental impact.

Hublot is committed to ethical gold sourcing and sustainable manufacturing processes. LVMH’s overarching commitment to sustainability is evident in its efforts to reduce waste, energy consumption, and environmental footprint throughout its watch production.

Swatch Group:

Swatch Group integrates sustainability into its watch brands through various initiatives. Omega is actively involved in marine conservation efforts, partnering with organizations like the GoodPlanet Foundation. Tissot focuses on responsible manufacturing and sustainable packaging, while Longines has initiatives to support equestrian sports and animal welfare.

Swatch Group’s commitment to sustainability is evident in its participation in ethical practices and its drive to contribute positively to society and the environment.

These companies are actively engaged in sustainability initiatives, demonstrating their commitment to environmental responsibility and ethical practices in the watch industry.

Consumer Perception and Loyalty:

Discuss the reputation of each company among consumers, brand loyalty, and the factors that contribute to their perceived value in the market.

LVMH (Moët Hennessy Louis Vuitton):

LVMH’s watch brands are synonymous with luxury, quality, and prestige. The conglomerate’s commitment to craftsmanship, innovation, and exclusivity fosters a perception of opulence and sophistication.

Loyal customers are drawn to the brand’s heritage and the unique stories behind each watch. The exclusivity of owning an LVMH timepiece contributes to strong brand loyalty among luxury enthusiasts who appreciate the artistry and history that each brand embodies.

Swatch Group:

Swatch Group’s diverse portfolio allows it to cater to a wide range of consumers, creating various degrees of loyalty. Swatch captures a youthful and fun-loving audience, fostering loyalty through its playful designs. Omega and Longines cultivate loyalty among enthusiasts who admire Swiss precision and heritage.

The association of Tissot with sports and Breguet with horological mastery contributes to loyal followings among specific interest groups.

Financial Performance:

LVMH (Moët Hennessy Louis Vuitton):

LVMH makes good money from its luxury watch brands, showing it’s a big player in the high-end market.

LVMH financial highlights 2022,

Luxury watches keep selling well, helping LVMH stay financially strong, thanks to its mix of fancy watch brands and other luxury goods.

Swatch Group:

Swatch Group’s financial performance is closely tied to its diverse brand portfolio and global reach. The company’s financial reports reveal a mix of revenue sources, ranging from entry-level to luxury watches.

Even with ups and downs in the market, Swatch Group does well because it sells both classic and trendy watches to various types of customers. This helps them stay steady in the industry.

How these companies do money-wise depends on market trends, what customers want, and how well they can keep up with new changes and ideas in the watch business.

Future Outlook

LVMH (Moët Hennessy Louis Vuitton):

LVMH’s future outlook in the watch industry remains promising as it continues to leverage its luxury heritage and innovation.

The conglomerate’s commitment to sustainability, coupled with its emphasis on craftsmanship, positions its watch brands to resonate with eco-conscious luxury consumers. The integration of technology and tradition, along with its portfolio of iconic brands, is likely to maintain LVMH’s strong presence in the evolving luxury watch market.

Swatch Group

Swatch Group’s future outlook is marked by its ability to balance tradition with innovation. As smartwatches gain popularity, the group’s diverse portfolio allows it to cater to a broader audience, including those seeking wearable technology.

Continued partnerships and collaborations, along with a focus on sustainability, are expected to contribute to Swatch Group’s relevance in the watch industry.

check Swatch groups visions: https://www.swatchgroup.com/en/swatch-group/swatch-group-history

Other Watch Groups

Fossil Group

Founded in 1984, with a 31-year history, the brand focuses on producing entry-level fashion watches at affordable prices. This strategy has garnered a vast customer base, dominating a significant share of the watch market. Headquartered in Richardson, Texas, the company specializes in crafting high-end timepieces, jewelry, sunglasses, wallets, and more.

Their ability to blend style, technology, and affordability has ensured a lasting presence in the industry, maintaining relevance with tech-savvy consumers through smartwatches and sustainable practices.

Citizen

Citizen holds a strong position in watchmaking, thanks to its unique solar-powered Eco-Drive technology. This tech makes their watches popular for both their cost and quality, offering great value. Even though many see Citizen as a brand for everyday watches, industry experts know they offer much more, including advanced technology.

The brand expanded by taking over other companies. In 2005, it acquired MIYOTA, known for its watch movements, and in 2008, it bought the American company Bulova, becoming a leader in quartz watches. The citizen then moved into the Swiss market in 2012 by purchasing Swiss brand Angelus and movement maker La Joux-Perret, as well as Arnold & Son watches. In 2016, Citizen grew again by acquiring the Frederique Constant brand, along with Alpina and DeMonaco.

Today, the Citizen group includes brands and products such as Citizen watches, Frederique Constant, Bulova, Arnold & Son, Alpina, Angelus, DeMonaco, MIYOTA movements, and La Joux-Perret movements.

Kering Group

Founded in 1963 by François Pinault as a building materials company, Kering transformed into a luxury group in the 1990s, shifting focus to luxury goods with key acquisitions like Gucci in 1999, followed by Yves Saint Laurent, Bottega Veneta, and Balenciaga. Kering values craftsmanship, evident in its acquisition of historic watchmakers Girard-Perregaux and Ulysse Nardin.

Known for its commitment to sustainability and corporate responsibility, Kering under Chairman and CEO François-Henri Pinault, emphasizes digital innovation and ethical business practices, positioning itself as a leader in the luxury sector with a broader influence on cultural and societal developments.

SEIKO Group

Seiko Holdings Corporation’s business areas include the production and distribution of watches, movements, and electronic components globally. In 1969, Seiko introduced the world’s first quartz analog watch, which nearly devastated the entire traditional Swiss watchmaking industry. Currently, it owns watch brands such as Seiko, Grand Seiko, Credor, Pulsar, Lorus, Alba, and Orient Star, as well as movement brands like the SII and Epson movements.

Movado Group

Movado Group, founded in 1983, is an esteemed designer, manufacturer, and distributor of watches. They encompass an array of brands such as the upscale Movado, known for its iconic Museum Watch that pioneered the minimalist aesthetic in watch design; Ebel, celebrated for its architectural lines; and MVMT, which caters to a more budget-conscious, fashion-forward audience.

They operate on a global scale, delivering an eclectic mix of timepieces that range from high-end luxury to accessible fashion statements. The group has built a reputation for strategic brand diversification, allowing it to touch different segments of the watch market while maintaining a steadfast commitment to quality and design across its brand portfolio.

Final Thoughts

As these brands occupy most of the market share of the watch industry, they are there to help us test the market, and have strong financial, human, and material resources to do market research, so from some of these brands the annual report of the daily newspaper, it can help us to understand the listed companies in the past year have done what?

How was the sales performance of the products?

How is the profit?

What are the changes in the internal and external competitive landscape?

What is the future development? What new products will there be?

Remember “Looking back, looking forward”, keeping up with the footsteps of big brands, we will walk faster and more steadily!

Discover key insights from the luxury market in 2022 and gain confidence in navigating this dynamic landscape. Explore valuable statistics on global luxury markets, LVMH’s financial performance, divisions, and competitors.

Explore 2022’s luxury market values, LVMH’s revenue surge to 79.2 billion euros, segment breakdowns, and competitive highlights.

Delve deeper into LVMH’s market share, regional revenue breakdowns, store growth, and advertising investment.

01 Market Overview

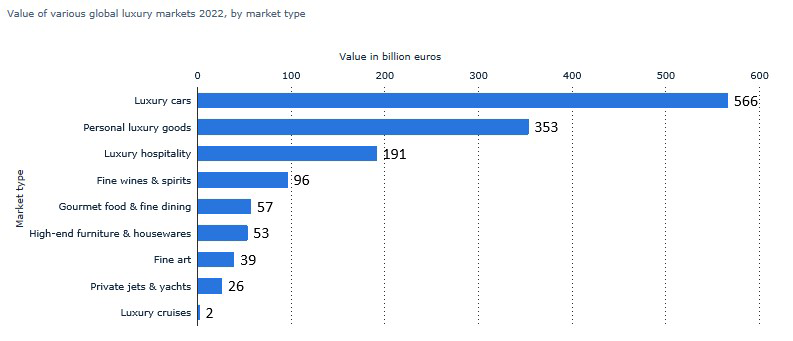

Value of various global luxury markets in 2022, by market type (in billion euros)

Descrição:This statistic shows the estimated value of various global luxury markets in 2022, by market type. It was estimated that in 2022 the global luxury cars market was worth about 566 billion euros. The total value of the global luxury goods market was approximately 1.38 trillion euros that year.

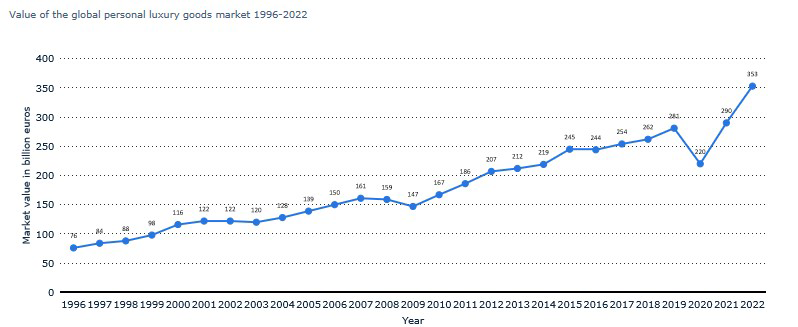

Value of the personal luxury goods market worldwide from 1996 to 2022 (in billion euros)

Descrição: This statistic shows the value of the personal luxury goods market worldwide from 1996 to 2022. In 2022, the value of the personal luxury goods market worldwide was estimated to be 353 billion euros.

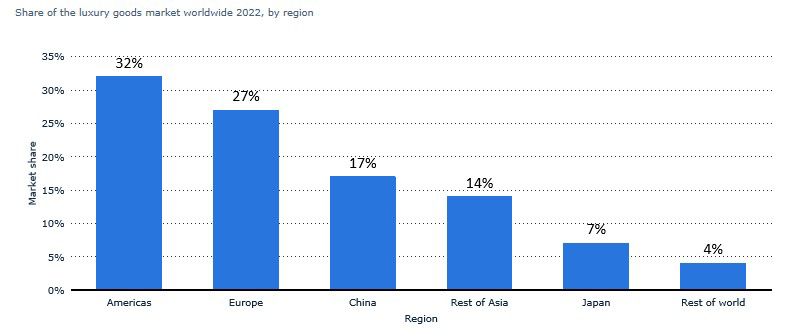

Share of the personal luxury goods market worldwide in 2022, by region

Descrição:This statistic shows the share of the personal luxury goods market worldwide in 2022, by region. In 2022, the Americas accounted for 32 percent of the global personal luxury goods market, followed by Europe with a share of 27 percent of the market.

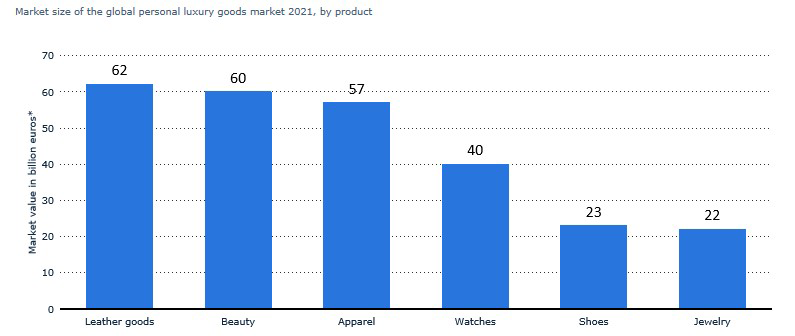

Personal luxury goods market value worldwide in 2021, by product type (in billion euros)

Descrição: This statistic shows the value of the personal luxury goods market worldwide in 2021, by product type. In 2021, the market value of personal luxury apparel products reached an estimated 57 billion euros.

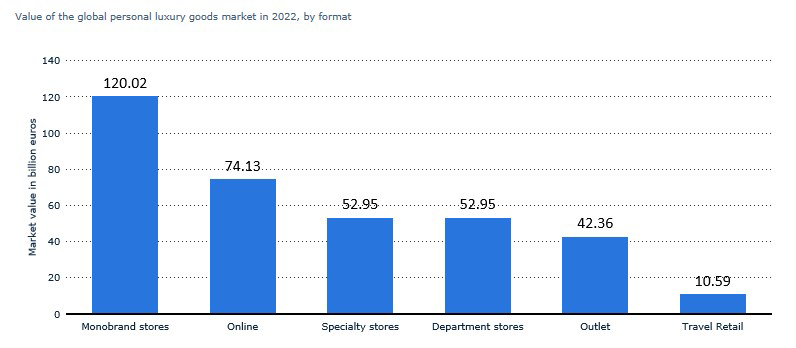

Value of the personal luxury goods market worldwide in 2022, by sales channel (in billion euros)

Descrição: This statistic shows the value of the personal luxury goods market worldwide in 2022, broken down by sales channel. In 2022, the value of the travel retail (airport) personal luxury goods market worldwide was roughly 11 billion euros.

Sales of the leading luxury companies worldwide from 2012 to 2021 (in billion euros)

Descrição:This statistic shows the sales of the leading luxury companies worldwide from 2012 to 2018, and provides a forecast from 2019 to 2021. In 2018, LVMH generated approximately 46.8 billion euros in sales worldwide.

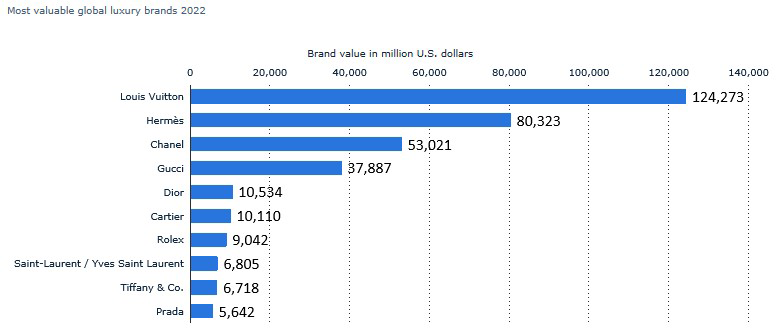

Brand value of the leading 10 most valuable luxury brands worldwide in 2022 (in million U.S. dollars)

Descrição: This statistic depicts the brand value of the leading 10 most valuable luxury brands worldwide in 2022. In that year, Chanel was the ninth most valuable luxury brand worldwide with a brand value of about 53 billion U.S. dollars.

Comment:Understanding the value of various luxury markets in 2022 provides a crucial baseline for assessing the potential of the luxury industry. The data on global luxury cars and personal goods markets presents a compelling narrative of consumer preferences. As a watch manufacturer, delving into these figures can help identify market gaps and opportunities to position your products effectively.

02 Financial performance

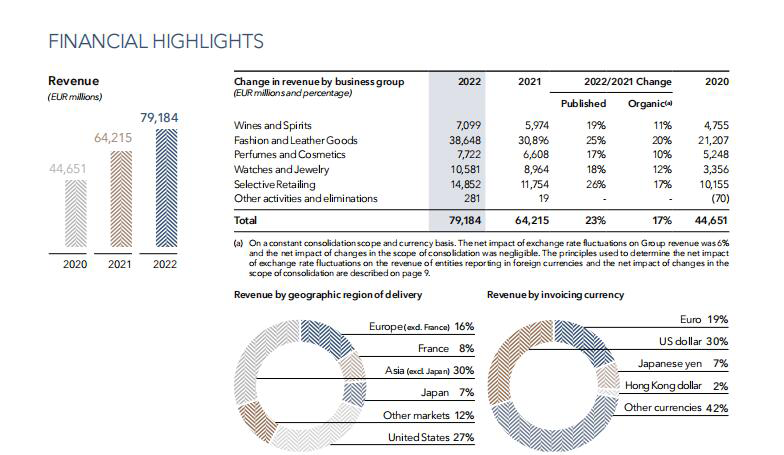

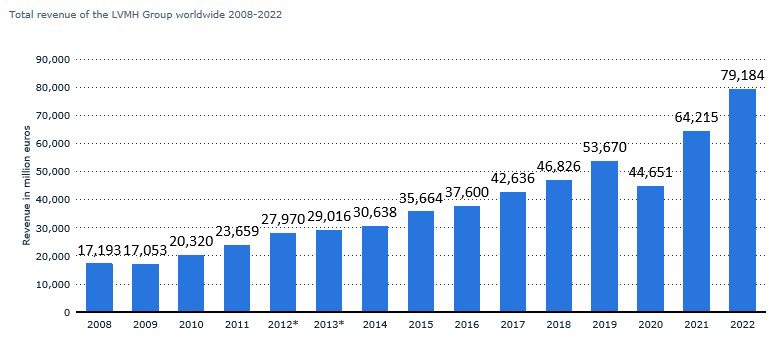

Total revenue of the LVMH Group worldwide from 2008 to 2022 (in million euros)

Descrição: Moët Hennessy Louis Vuitton (LVMH) is one of the world`s leading luxury groups, parent to 75 luxury houses. Over the past decade, LVMH enjoyed ever-increasing global revenue, reaching over 53 billion euros in 2019. In 2022, bouncing fully back from the impact of the coronavirus (COVID-19) pandemic, the group`s revenue saw an increase of about 77 percent on 2022, ultimately amounting to 79.2 billion euros for the year.

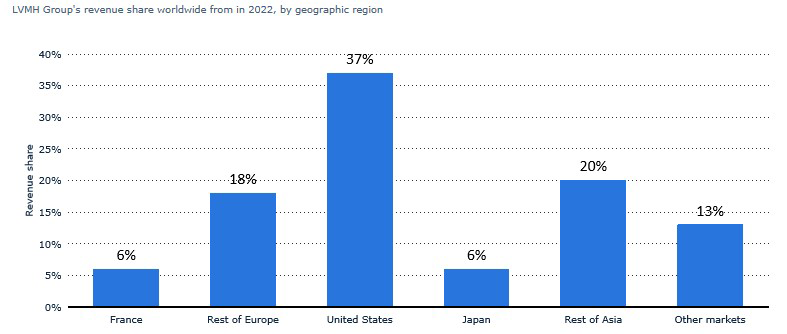

Revenue share of the LVMH Group worldwide in 2022, by geographic region

Descrição: This statistic shows the revenue share of the LVMH Group worldwide in 2022, by geographic region. In 2022, LVMH Group’s global revenue share from the United States was 37 percent.

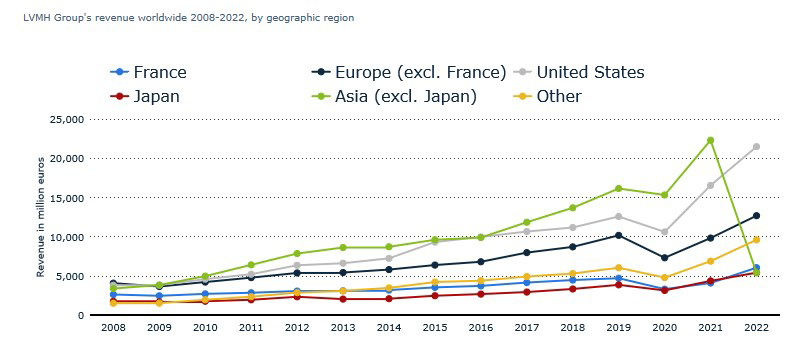

Revenue of the LVMH Group worldwide from 2008 to 2022, by geographic region (in million euros)

Descrição: This statistic shows the revenue of the LVMH Group worldwide from 2008 to 2022, broken down by geographic region. In 2022, the LVMH Group generated approximately 21.6 billion euros in revenues in the United States. The company had total revenues of 79.2 billion euros that year.

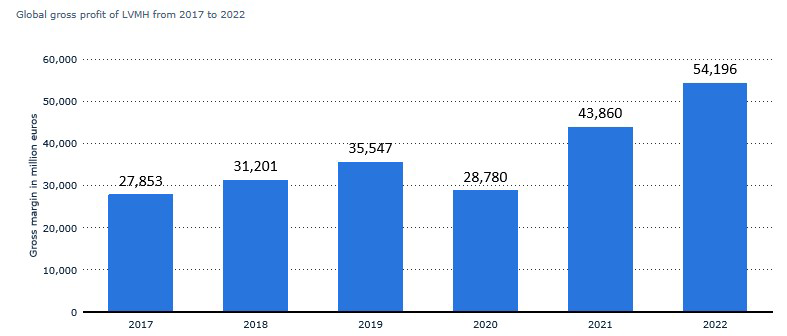

Gross margin of the LVMH Group worldwide from 2017 to 2022 (in million euros)

Descrição: In 2022, LVMH had a gross margin of 54.2 billion euros. The LVMH Group is a French luxury goods corporation, which owns 75 luxury brands worldwide, including Louis Vuitton, Moët, Hennessy, and Bulgari.

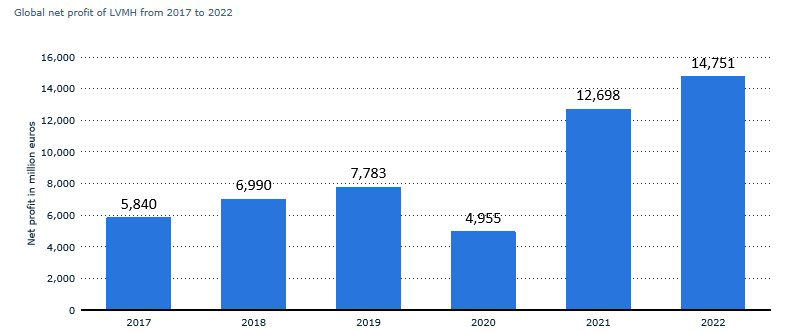

Net profit of the LVMH Group worldwide from 2017 to 2022 (in million euros)

Descrição: In 2022, LVMH had a gross margin of 54.2 billion euros. The LVMH Group is a French luxury goods corporation, which owns 75 luxury brands worldwide, including Louis Vuitton, Moët, Hennessy, and Bulgari.

Comment:

LVMH’s financial trajectory showcases resilience and adaptability in a dynamic market landscape. The significant revenue surge in 2022 underscores the importance of agility and innovation, especially in post-pandemic recovery. Examining the revenue share by geographic region adds depth to understanding LVMH’s global market strategy, aiding in strategic partnerships and expansion plans.

03 Divisions

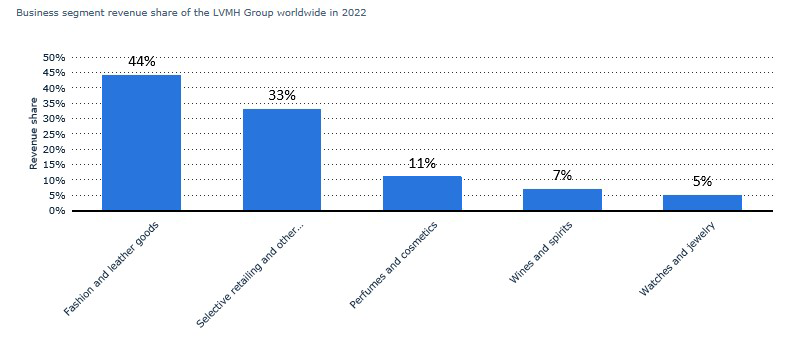

Revenue share of the LVMH Group worldwide in 2022, by business segment

Descrição: This statistic shows the revenue share of the LVMH Group worldwide in 2022, by segment. In 2022, 44 percent of the LVMH Group’s global revenue came from the company’s fashion and leather goods business segment.

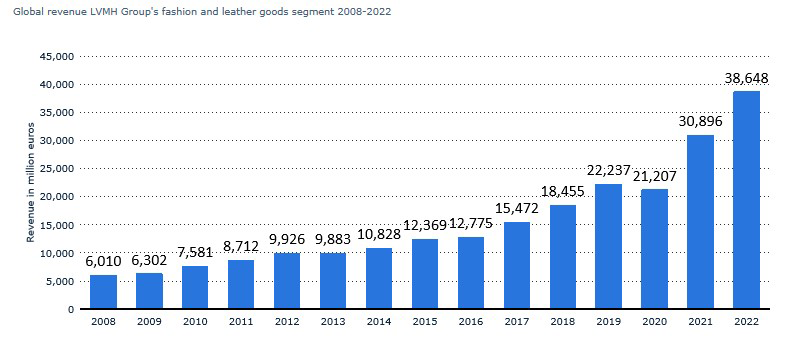

Global revenue of LVMH Group’s fashion and leather goods segment from 2008 to 2022 (in million euros)

Descrição:The Louis Vuitton brand is the backbone of the French luxury conglomerate LVMH`s fashion and leather goods segment, but the group is home to many other iconic luxury brands and fashion houses as well. Christian Dior, Fendi, Marc Jacobs, and Givenchy, among others, all operate under LVMH`s fashion and leather goods segment, which reported a sales revenue of approximately 38.7 billion in 2022.

Global revenue of LVMH Group’s fashion and leather goods segment from 2008 to 2022 (in million euros)

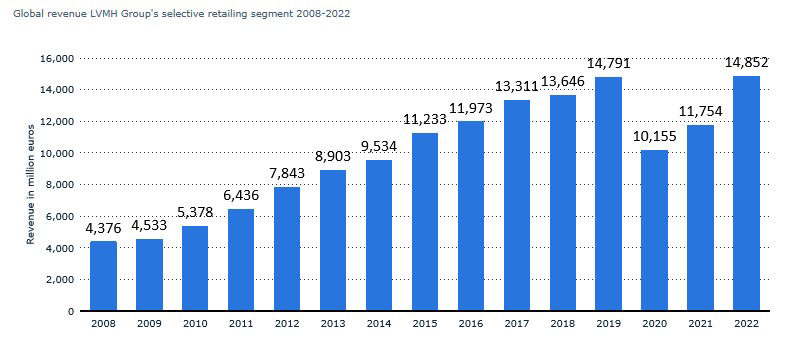

Descrição: This statistic shows the global revenue of LVMH Group’s selective retailing segment from 2008 to 2022. In 2022, this segment generated revenues of 14.9 billion euros, an increase of over three billion euros compared to 2021. The LVMH Group is a French luxury goods corporation, which owns around 75 luxury brands worldwide, including Louis Vuitton and Bulgari. The fashion and leather goods segment generates the most revenue for LVMH.

Global revenue of LVMH Group’s perfumes and cosmetics segment from 2008 to 2022 (in million euros)

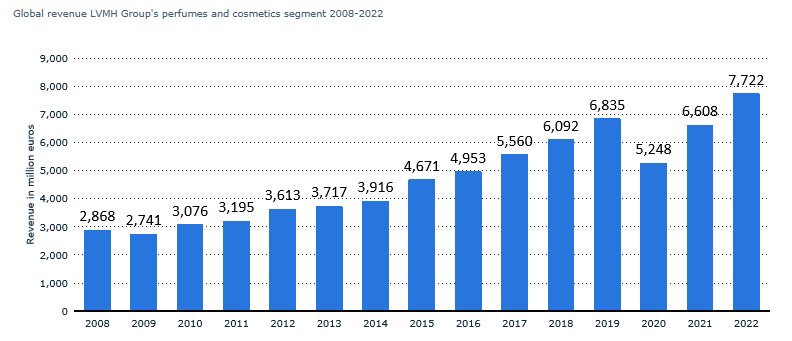

Descrição: This statistic shows the global revenue of LVMH Group’s perfumes and cosmetics segment from 2008 to 2022. In 2022, this segment generated revenues of 7.7 billion euros, which was an increase of more than one billion euros compared to the previous year. The LVMH Group is a French luxury goods corporation, which owns around 75 luxury brands worldwide, including Louis Vuitton and Bulgari. The fashion and leather goods segment generates the most revenue for LVMH.

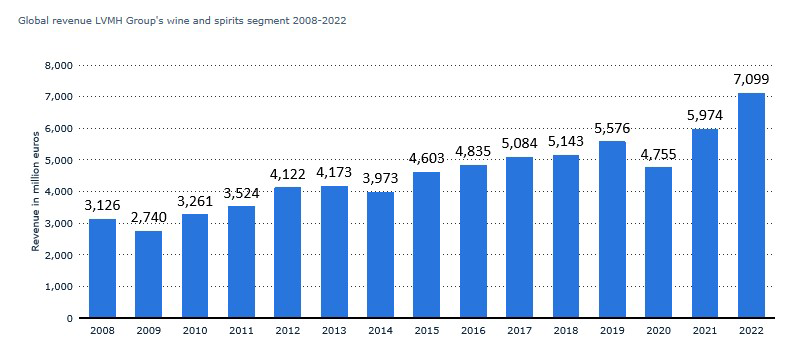

Global revenue of LVMH Group’s wine and spirits segment from 2008 to 2022 (in million euros)

Descrição:This statistic shows the global revenue of LVMH Group’s wine and spirits segment from 2008 to 2022. In 2022, this segment generated a global revenue of approximately seven billion euros, an increase of more than 1.2 billion euros compared to 2021. The LVMH Group is a French luxury goods corporation, which owns around 75 luxury brands worldwide, including Louis Vuitton and Bulgari. The fashion and leather goods segment generates the most revenue for LVMH.

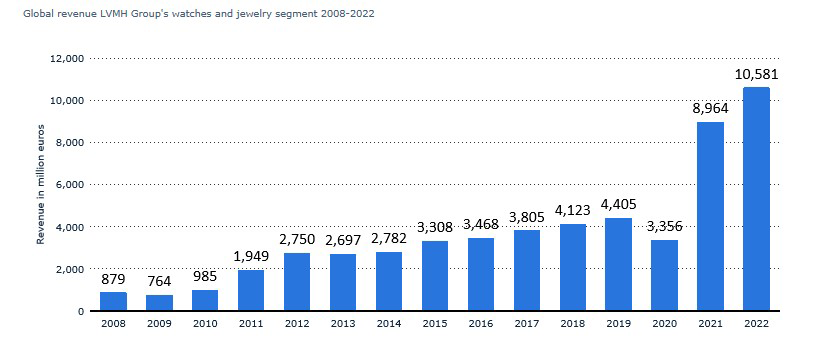

Global revenue of LVMH Group’s watches and jewelry segment from 2008 to 2022 (in million euros)

Descrição:This statistic shows the global revenue of LVMH Group’s watches and jewelry segment from 2008 to 2022. In 2022, this segment generated revenues of approximately 10.6 billion euros, which was more than double the revenue registered in 2020. The LVMH Group is a French luxury goods corporation, which owns around 50 luxury brands worldwide, including Louis Vuitton and Bulgari. The fashion and leather goods segment generates the most revenue for LVMH.

Comment:The prominence of LVMH’s fashion and leather goods segment speaks to the enduring allure of personal luxury items. Diversification into perfumes, cosmetics, watches, and jewelry provides insights into evolving consumer preferences. For your watch manufacturing business, this insight underscores the need to align with consumer trends and capitalize on segments with growth potential.

04 Key company figures

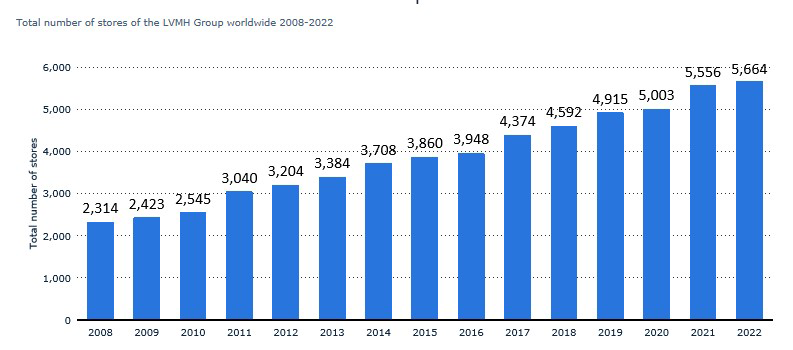

Total number of stores of the LVMH Group worldwide from 2008 to 2022

Descrição: LVMH had a total of 5,664 stores in operation around the world as of 2022, up from 2,314 in 2008. LVMH, an amalgamation of Louis Vuitton, Moët, and Hennessy, is the top selling luxury personal goods companies in the world. The company operates globally selling a diverse range of products. LVMH sells luxury leather goods, handbags, and ready-to-wear fashion through its Louis Vuitton brand, and wines and spirits through its Moët and Hennessy brands.

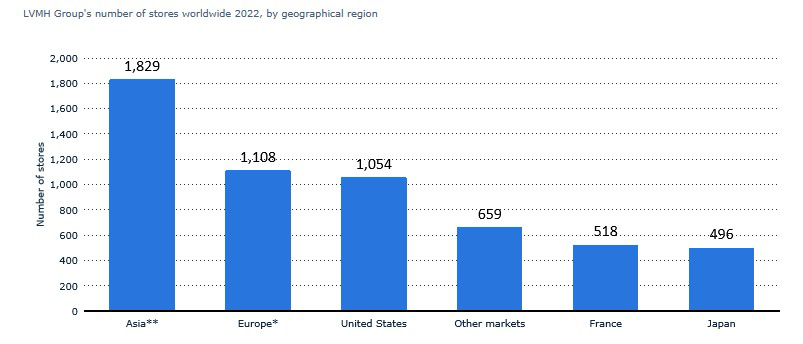

Number of stores of the LVMH Group worldwide in 2022, by geographical region

Descrição: This statistic shows the number of stores of the LVMH Group worldwide in 2022, by geographical region. In that year, the total number of stores the LVMH Group had throughout the United States was 1,054.

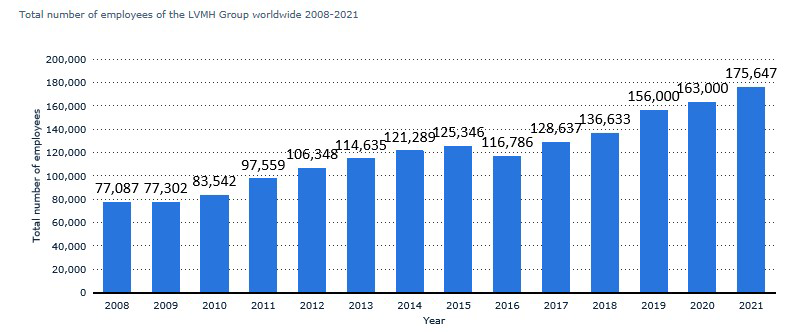

Total number of employees of the LVMH Group worldwide from 2008 to 2021

Descrição: This statistic shows the number of stores of the LVMH Group worldwide in 2022, by geographical region. In that year, the total number of stores the LVMH Group had throughout the United States was 1,054.

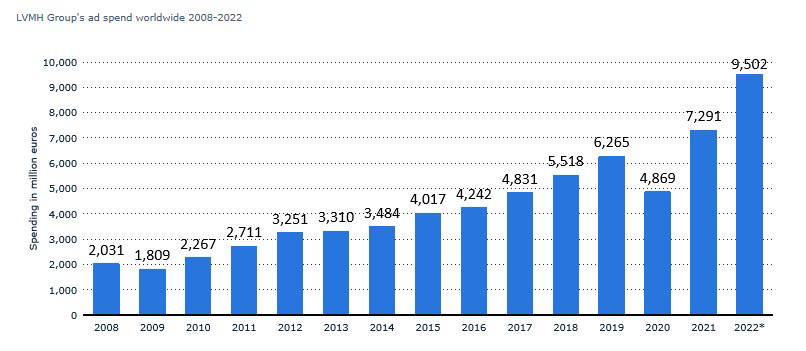

Advertising and promotion expenditure of the LVMH Group worldwide from 2008 to 2022 (in million euros)

Descrição: The French luxury goods conglomerate LVMH Group spent around 9.5 billion euros in advertising and promotion costs worldwide as of 2022, reaching an all-time higher investment on advertising since 2008. Primarily known for its fashion house Louis Vuitton, the LVMH Group invested about 7.3 billion euros in advertising in 2021.

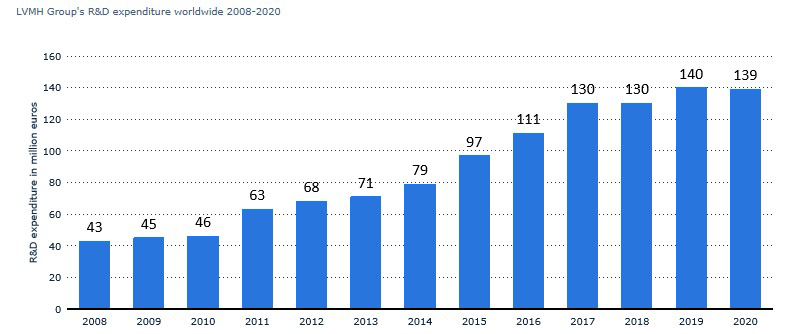

Research and development (R&D) expenditure of the LVMH Group worldwide from 2008 to 2020 (in million euros)

Descrição: This statistic highlights the trend in research and development (R&D) expenditure of the LVMH Group worldwide from 2008 to 2020. In 2019, LVMH Group’s global R&D expenditure amounted to about 139 million euros.

Comment:LVMH’s exponential growth in store count signifies effective market penetration and customer engagement. The substantial investment in advertising and promotion reflects a commitment to brand resonance. The emphasis on research and development indicates a forward-looking approach, vital for maintaining innovation and competitiveness in a rapidly evolving luxury landscape.

05 Competitors

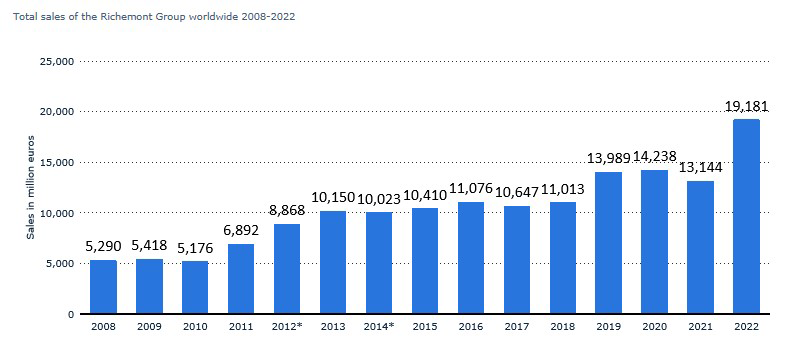

Total sales of the Richemont Group worldwide from FY2008 to FY2022 (in million euros)

Description: In FY2011, total sales of the Richemont Group worldwide amounted to about 19.18 billion euros, increasing by approximately six billion euros on the previous year. The Richemont Group is one of the leading luxury goods companies in the world. The Richemont Group garnered most of its revenue from jewelry Maisons in FY2022, which amounted to around 11 billion euros. The Asia-Pacific was responsible for 40.77 percent of the company`s total sales that year.

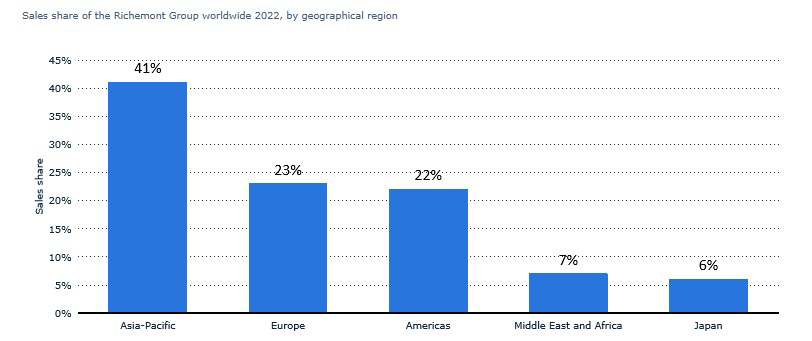

Sales share of the Richemont Group worldwide in FY2022, by geographical region

Descrição: This timeline shows the sales share of the Richemont Group worldwide in the financial year 2022, by geographical region. In that year, the sales share of the Richemont Group’s European region amounted to about 23 percent.

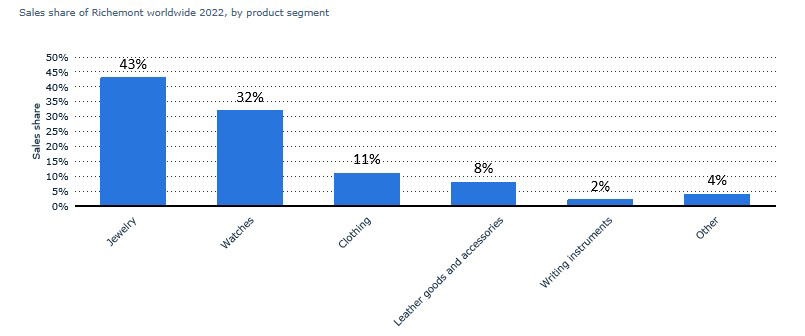

Richemont Group’s sales share worldwide in 2022, by product category

Descrição: In the financial year 2022, watch and jewelry sales accounted for about 75 percent of Richemont’s global sales. The company had total sales of approximately 19.18 billion euros that year.

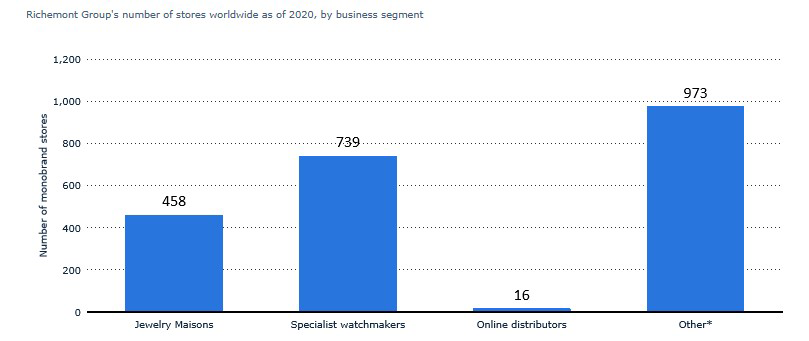

Total number of monobrand stores of the Richemont Group worldwide as of 2020, by business area

Descrição: As of September 30, 2020, the jewelry maison division of Richemont Group operated 458 monobrand stores around the world. Richemont owns a number of luxury brands, such as Cartier, Van Cleef & Arpels, and Buccellati.

Revenue share of the Kering Group worldwide in 2022, by region

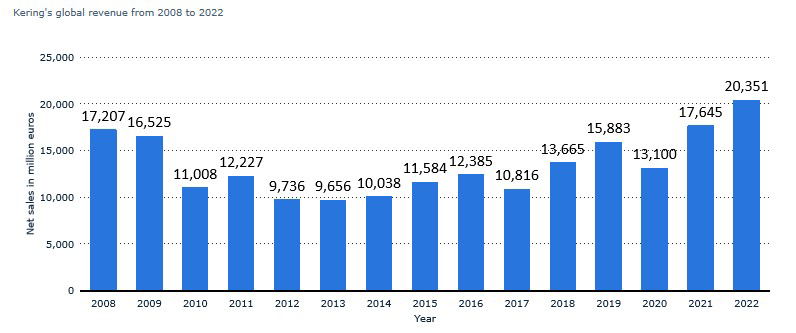

Descrição: This timeline depicts the global revenue of the Kering Group from 2008 to 2022. In 2022, Kering’s global revenue amounted to about 20.4 billion euros.

Revenue of the Kering Group worldwide from 2008 to 2022 (in million euros)

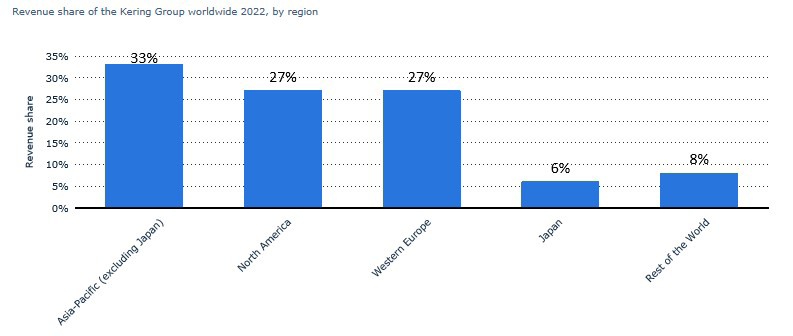

Descrição: In 2022, 27 percent of the Kering Group’s revenue was generated from the North American region. The company’s total revenue amounted to approximately 20.35 billion euros that year.

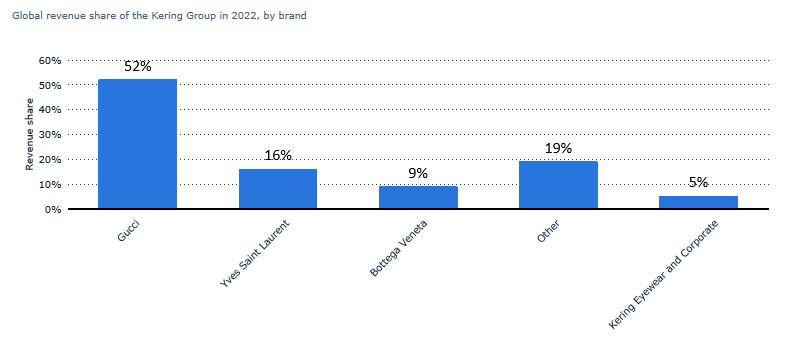

Revenue share of the Kering Group worldwide in 2022, by brand

Descrição: In 2022, the Gucci brand generated 52 percent of the Kering Group’s global revenue. Kering’s global revenue was approximately 20.35 billion euros that year.

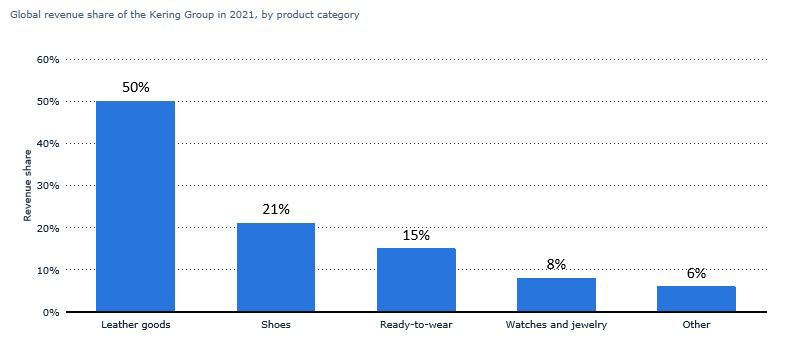

Revenue share of the Kering Group worldwide in 2021, by product category

Descrição:In 2021, the leather goods product category accounted for half of the Kering Group’s global revenue. Kering’s global revenue was approximately 17.64 billion euros that year.

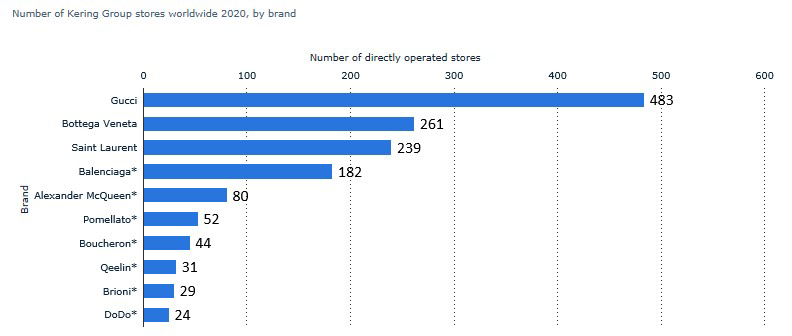

Number of directly operated Kering Group stores worldwide in 2020, by brand

Descrição:In 2021, the leather goods product category accounted for half of the Kering Group’s global revenue. Kering’s global revenue was approximately 17.64 billion euros that year.

Comment:Studying competitors like Richemont and Kering sheds light on diverse luxury market players. Richemont’s focus on jewelry and Kering’s emphasis on brands like Gucci illuminate niche strategies. Understanding their sales distribution and product mix can inform your approach, aiding in identifying unique selling points and ways to differentiate your watches.

Pensamento final

With a pulse on luxury market dynamics, LVMH’s success story and strategic insights provide a compass for your journey in the world of luxury watches

The jewelry industry in Italy has experienced remarkable growth and transformation in recent years. From the steady increase in turnover and production value to the impact of global market trends and consumer behavior, the Italian jewelry sector continues to thrive.

In this article, we delve into various aspects of the industry, including revenue trends, leading companies, international trade, and consumer behavior, shedding light on the dynamic nature of the Italian jewelry market.

01 Italian jewelry industry

Receita dos relógios & jewelry industry Worldwide 2017-2026 (in billiondólares americanos)

Descrição:The global revenue in the watches & jewelry segment of the accessories market was forecast to continuously increase between 2023 and 2026 by in total 44.8 billion U.S. dollars (+11.97 percent). The revenue is estimated to amount to 418.9 billion U.S. dollars in 2026.

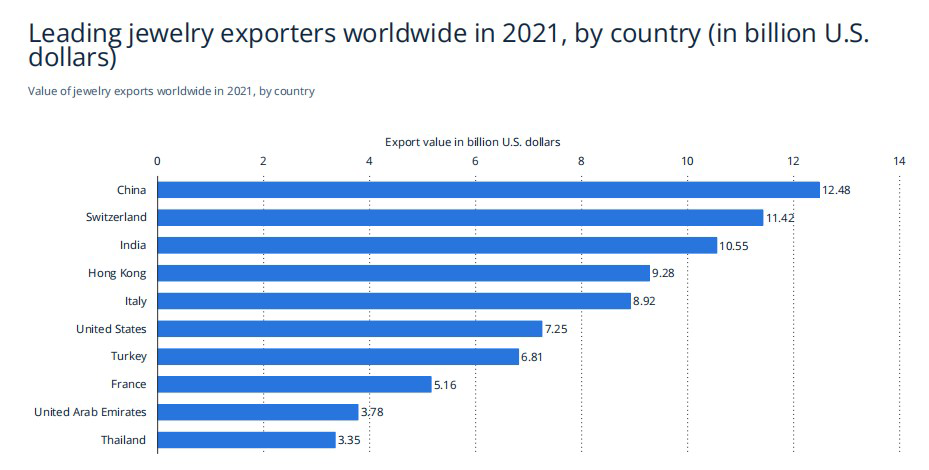

Leading jewelry exporters worldwide in 2021, by country (in billion U.S.dollars)

Descrição:This statistic shows the value of jewelry exports from the leading countries worldwide in 2021. In 2021, Switzerland exported approximately 11.4 billion U.S. dollars of jewelry around the world, which was slightly less than top-placed United States.

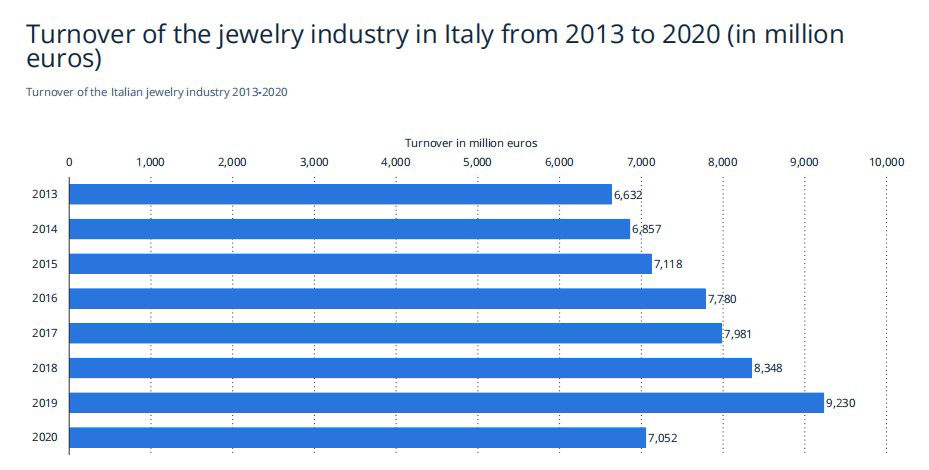

Turnover of the jewelry industry in Italy from 2013 to 2020 (in millioneuros)

Descrição:This statistic displays the turnover of the jewelry industry in Italy from 2013 to 2019. According to the data, over the period of consideration, the turnover of the jewelry industry in Italy grew steadily, going from approximately 6.6 billion euros in 2013 to almost 9.2 billion euros in 2019.

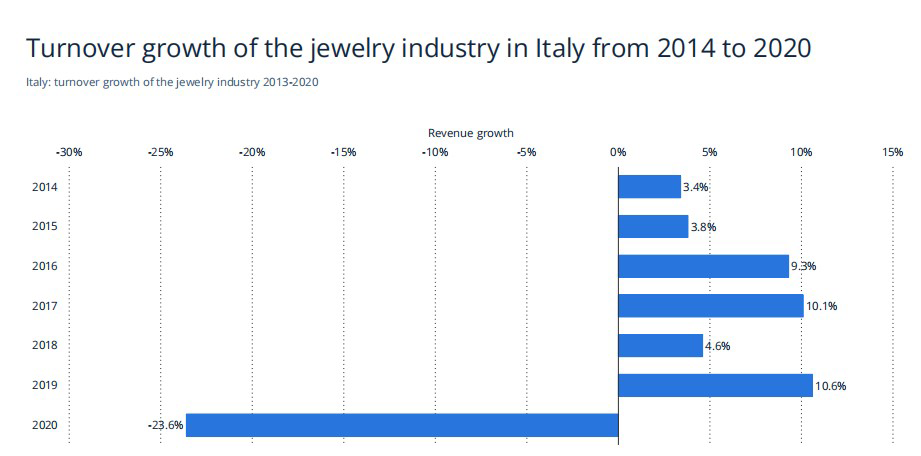

Turnover growth of the jewelry industry in Italy from 2014 to 2020

Descrição:This statistic displays the growth of the turnover of the jewelry industry in Italy from 2014 to 2020. According to the data, over the period of consideration, the turnover of the jewelry industry in Italy grew steadily, peaking at more 10.6 percent in 2019, up from the previous years.

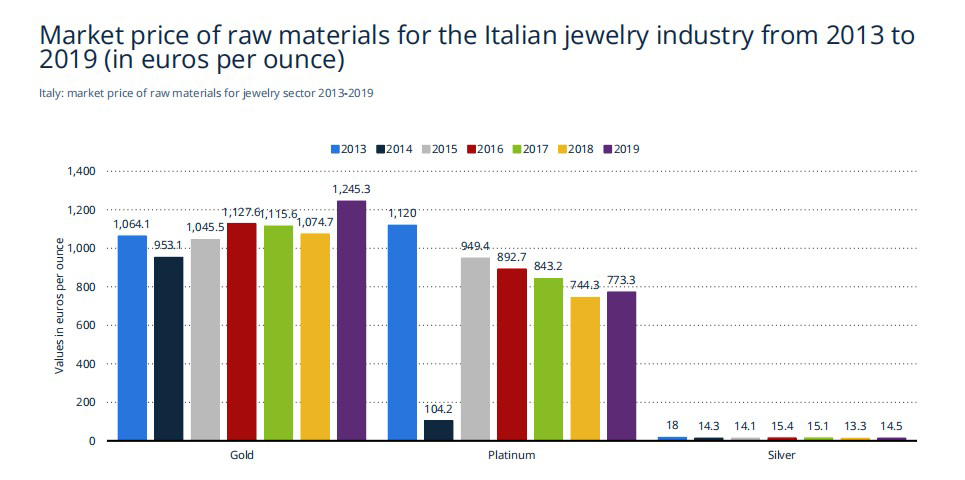

The market price of raw materials for the Italian jewelry industry from 2013 to 2019 (in euros per ounce)

Descrição: This statistic displays the market price of raw materials for the Italian jewelry industry in Italy between 2013 and 2019. As of the survey period, the market price of gold fluctuated over time reaching its lowest value in 2014 at 953.1 euros per ounce and peaked at 1,128 euros in 2016.

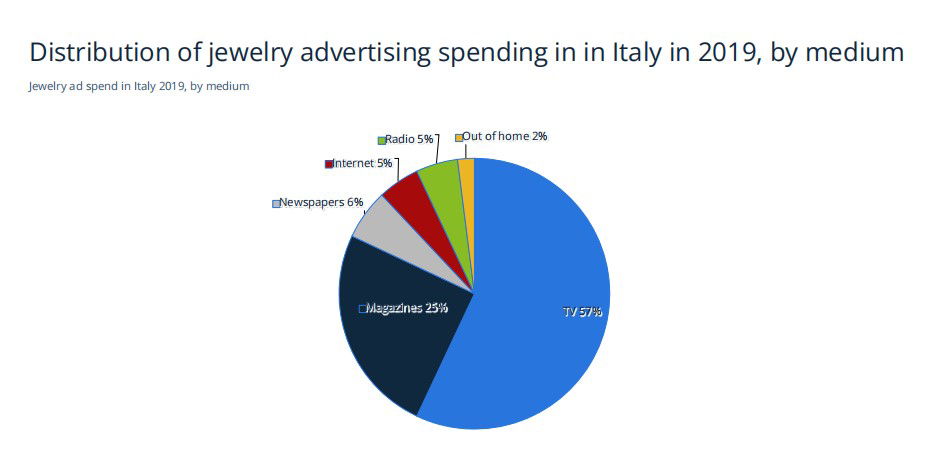

Distribution of jewelry advertising spending in in Italy in 2019, by medium

Descrição:In 2019, 57 percent of advertising investments of jewelry brands in Italy were destined towards TV ads. Magazines were the second most popular medium, with 25 percent. Italian jewelry industry invested a total of 59.4 million euros in advertising thatyear.

02 Leading companies

Leading watches and jewelry companies in Italy in 2020, by sales revenues(in 1,000 euros)

Descrição:This statistic presents the leading companies active in the manufacturing/distribution of watches and jewelry in Italy in 2019, by sales revenues.

According to data provided by Competitive Data, in 2020, LVMH Italia S.p.A. was the leadingmanufacturer/distributor of watches and jewelry in Italy, with domestic sales revenues of 718 million euros. Following in the ranking came Bulgari, with domestic revenue of 412 million euros.

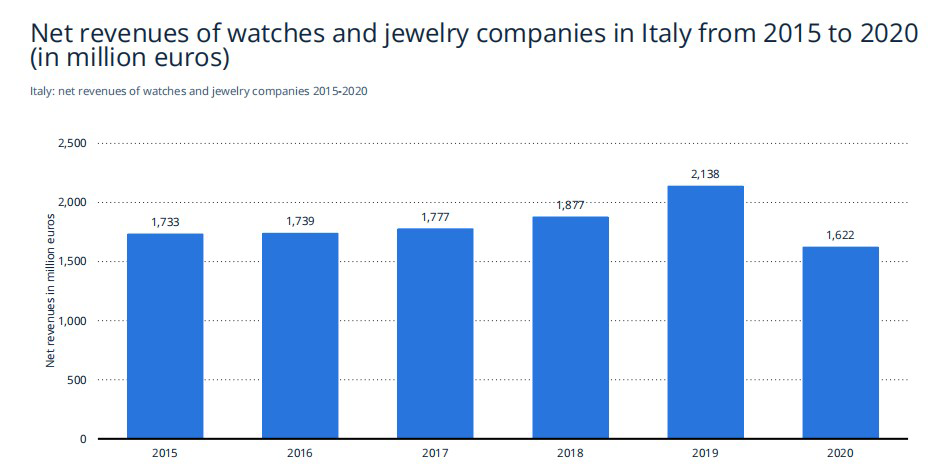

Net revenues of watches and jewelry companies in Italy from 2015 to 2020(in million euros)

Descrição:This statistic presents the net revenues of a significant sample of companies active in the manufacturing/distribution of watches and jewelry in Italy from 2015 to 2020. According to data provided by Competitive Data, domestic net revenues of the companies sampled in Italy increased from 1.7 billion euros in 2015 to 2.1 billion euros in 2019, before dropping again to 1.6 million euros in 2020.

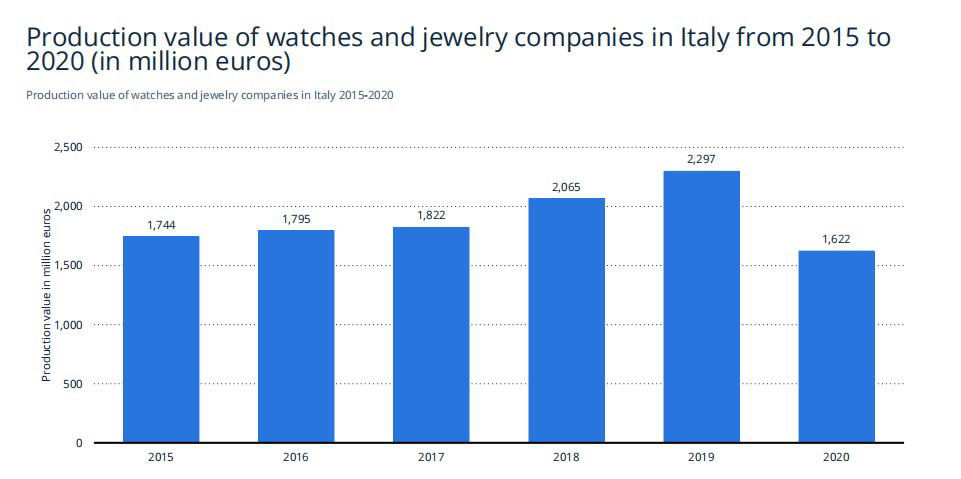

Production value of watches and jewelry companies in Italy from 2015 to2020 (in million euros)

Descrição:This statistic presents the production value of a significant sample of companies active in the manufacturing/distribution of watches and jewelry in Italy from 2015 to 2020. According to data provided by Competitive Data, production value of thecompanies sampled in Italy increased from 1.74 billion euros in 2015 to over 2.2 billion euros in 2019. This value decline in 2020 to 1.6 milion euros.

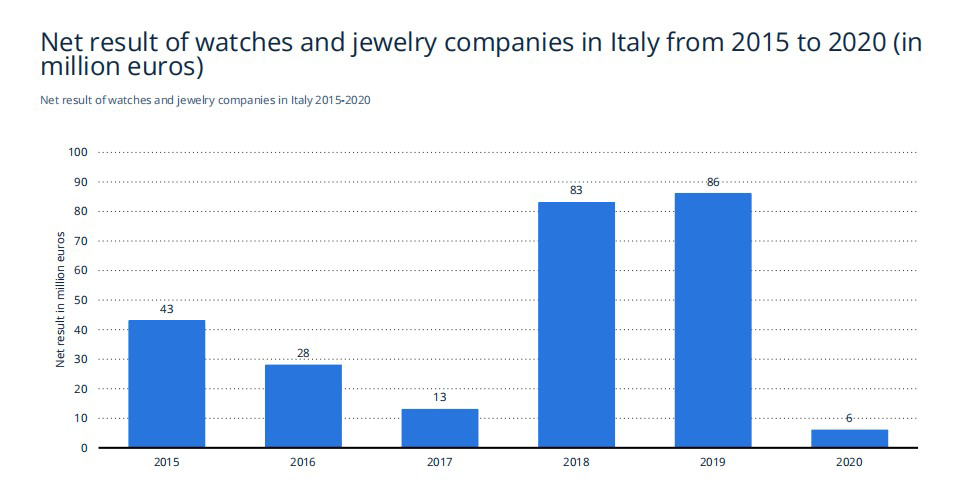

Net result of watches and jewelry companies in Italy from 2015 to 2020 (inmillion euros)

Descrição:This statistic presents the net result of a significant sample of companies active in the manufacturing/distribution of watches and jewelry in Italy from 2015 to 2020. According to data provided by Competitive Data, net result of the companies sampled inItaly decreased from 43 million euros in 2015 to 86 million euros in 2019. In 2020, this figure declined to six million euros.

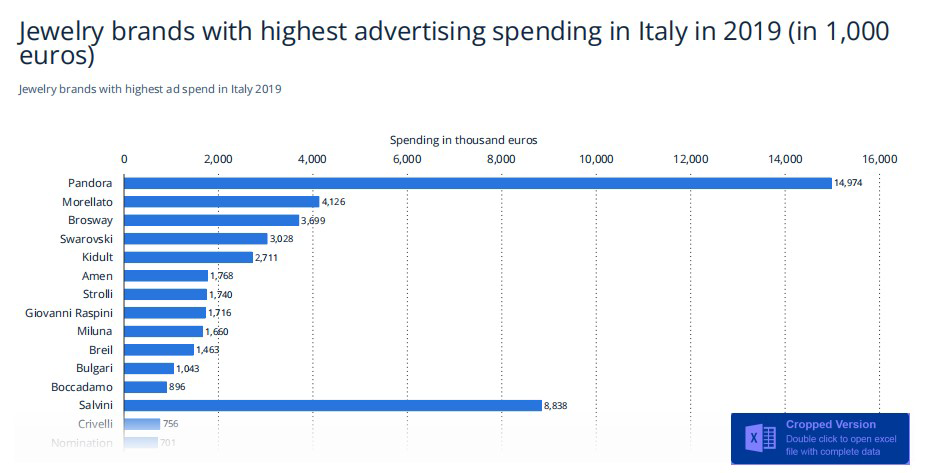

Jewelry brands with highest advertising spending in Italy in 2019 (in 1,000 euros)

Descrição:In 2019, Pandora was the jewelry brand with highest advertising spending in Italy. Its ad expenditures amounted to 14.97 million euros, more than 3.5 times more than Morellate, which ranked second. Italian jewelry industry invested a total of 59.4 million euros in advertising that year.

03 International trade

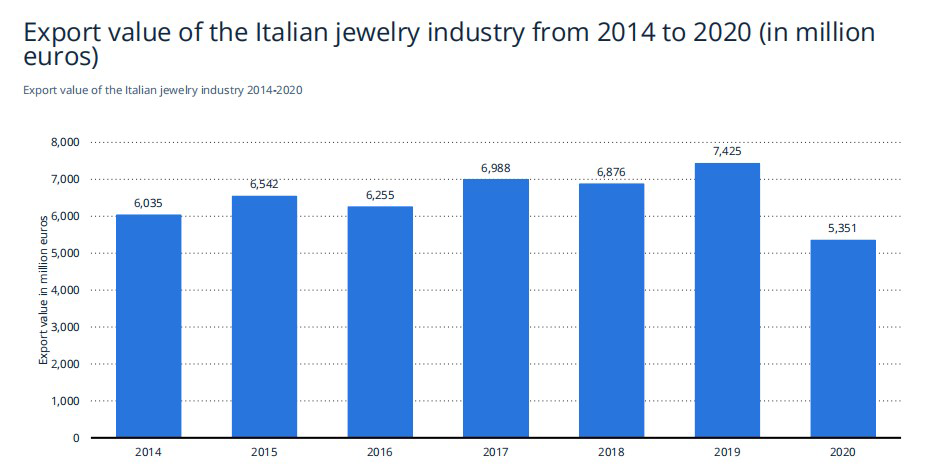

Export value of the Italian jewelry industry from 2014 to 2020 (in millioneuros)

Descrição:This statistic displays the export value of the Italian jewelry industry from 2014 to 2020. According to the data, during the period of consideration, the value of the exports of the Italian jewelry industry increased overall, growing from approximately six billion euros in 2014 to just over 7.4 billion euros in 2019.

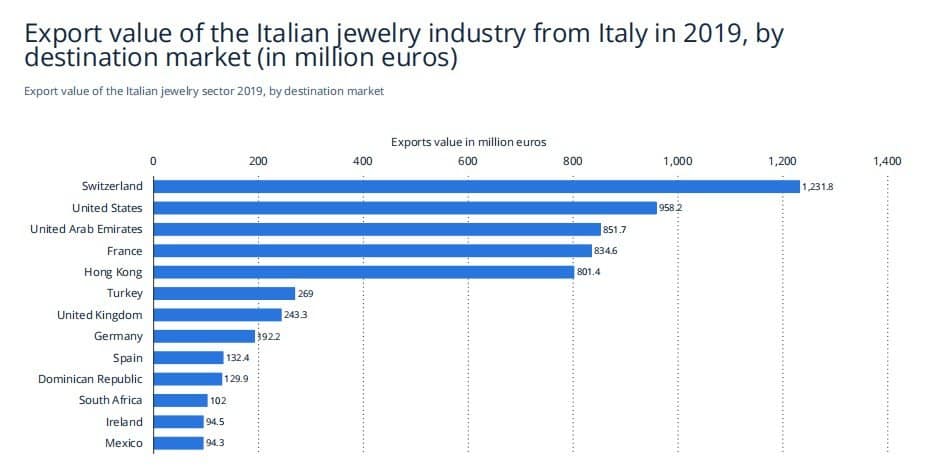

Export value of the Italian jewelry industry from Italy in 2019, bydestination market (in million euros)

Descrição:In 2019, the value of the export of the Italian jewelry industry to the Swiss market amounted to about 1.2 billion euros. Export of the Italian jewelry industry to the U.S. market followed with a total export value of 958.2 million euros.

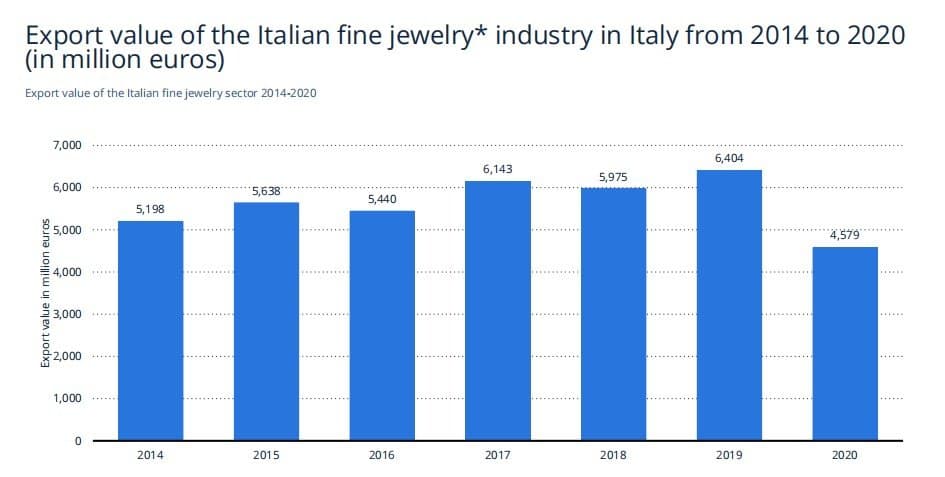

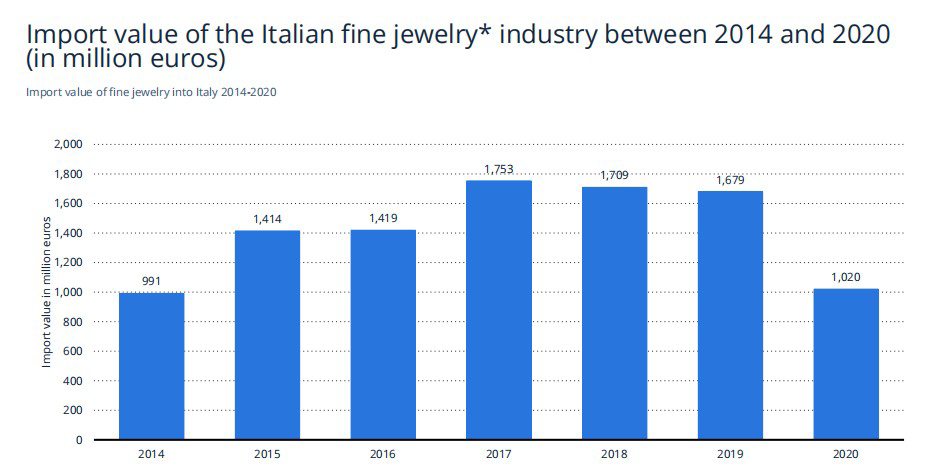

Export value of the Italian fine jewelry industry in Italy from 2014 to 2020(in million euros)

Descrição:This statistic displays the export value of the Italian fine jewelry industry in Italy between 2014 and 2020. As of the survey period, the value of the export of the Italian fine jewelry industry increased from about 5.2 billion euros in 2014 to approximately 6.4billion euros in 2019.

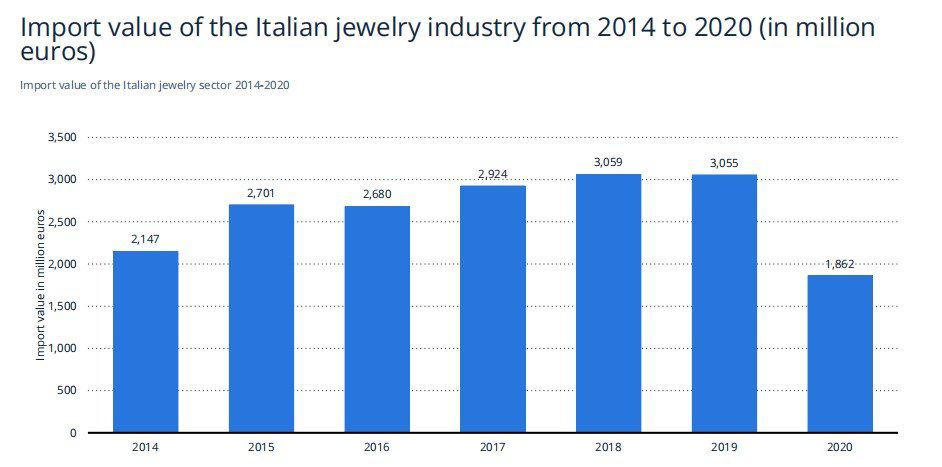

Import value of the Italian jewelry industry from 2014 to 2020 (in millioneuros)

Descrição:This statistic displays the import value of the Italian jewelry industry in the period from 2014 to 2020. The value of imports of the Italian jewelry industry increased from about 2.1 billion euros in 2014 to about 3.1 billion euros in 2019.

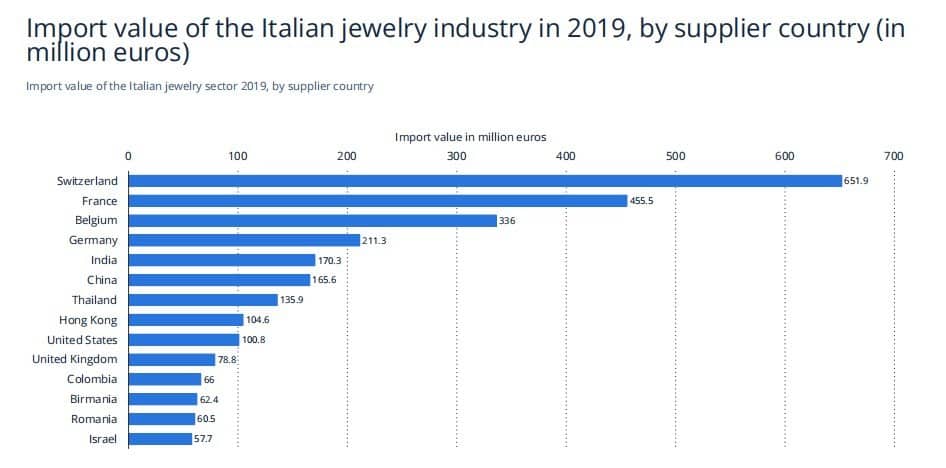

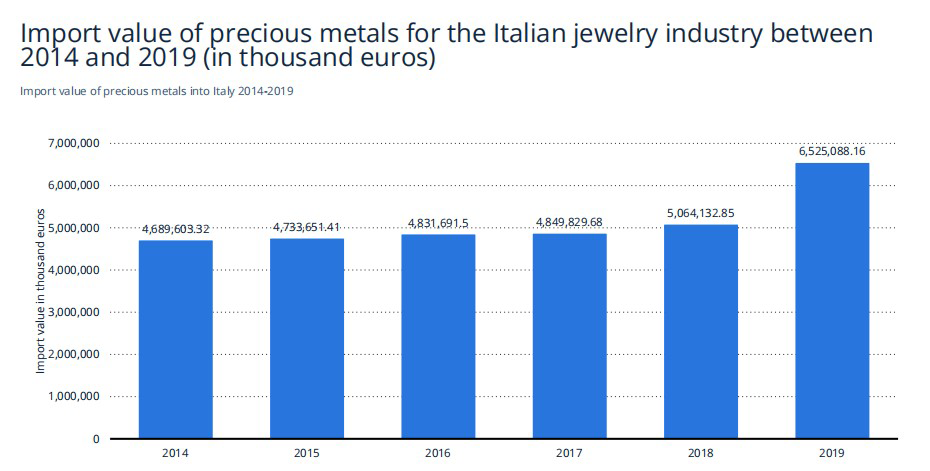

Import value of the Italian jewelry industry in 2019, by supplier country (inmillion euros)